Braceland Homes Inc. is an Escondido, CA real estate brokerage founded in 2018 by retired US Navy officer Erik Braceland (DRE 02059069). Erik launched his second career after several underwhelming experiences with REALTORS® he worked with to buy and sell his own investment properties while serving on active duty. His systems, processes, and strategies positively impact the way homes are sold, and the systematic trademarked approach he embraces, guarantees his clients' satisfaction and success.

In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5.25%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

How Rising Mortgage Rates Impact You

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase even more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with one of our trusted real estate advisors at Braceland Homes. We can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Call or text us at 619-947-3560 so you can better understand your budget and be prepared to buy your home even before rates climb higher.

The link between financial security and homeownership is especially important today as inflation rises. But many people may not realize just how much owning a home contributes to your overall net worth. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

"Homeownership is rewarding in so many ways and can serve as a vital component in achieving financial stability."

Here are just a few reasons why, if you’re looking to increase your financial stability, homeownership is a worthwhile goal.

Owning a Home Is a Building Block for Financial Success

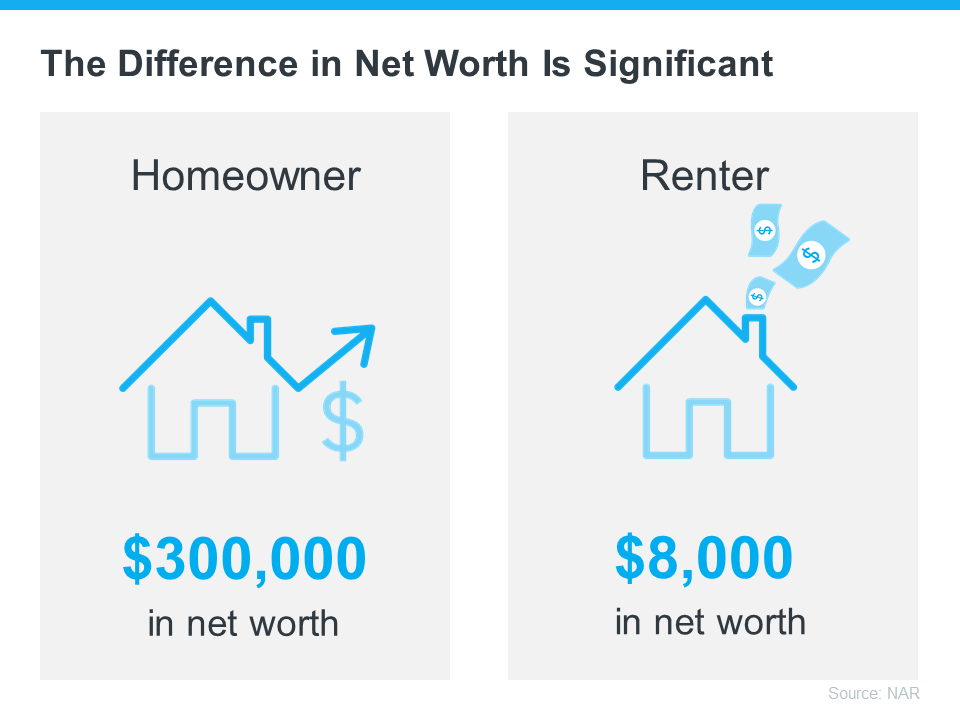

A recent NAR report details several homeownership trends and statistics, including the difference in net worth between homeowners and renters. It finds:

“. . . the net worth of a homeowner was about $300,000 while that of a renter’s was $8,000 in 2021.”

To put that into perspective, the average homeowner’s net worth is roughly 40 times that of a renter(see visual below):

The results from this report show that owning a home is a key piece to the puzzle when building your overall net worth.

Equity Gains Can Substantially Boost a Homeowner’s Net Worth

The net worth gap between owners and renters exists in large part because homeowners build equity. As a homeowner, your equity grows as your home appreciates in value and you make your mortgage payments each month.

In other words, when you own your home, you have the benefit of your mortgage payment acting as a contribution to a forced savings account. And when you sell, any equity you’ve built up comes back to you. As a renter, you’ll never see a return on the money you pay out in rent every month.

To sum it up, NAR says it simply:

“Homeownership has always been an important way to build wealth.”

Bottom Line

The gap between a homeowner’s net worth and a renter’s shows how truly foundational homeownership is to wealth-building. If you’re ready to start on your journey to homeownership, call us at Braceland Homes today 619-947-3560.

Why work with a real estate agent? Because buying or selling a home is such a big decision in our lives, the need for clear, trustworthy information and guidance is crucial. And while no one can give you perfect advice, when you align yourself with real estate experts, like those at Braceland Homes, you’ll get the best advice for your situation.

An Expert Will Give You the Best Advice Possible

Let’s say you need an attorney, so you seek out an expert in the type of law required for your case. When you go to their office, they won’t immediately tell you how the case is going to end or how the judge or jury will rule. What a good attorney can do, though, is discuss the most effective strategies you can take. They may recommend one or two approaches they believe will work well for your case.

Then, they’ll leave you to make the decision on which option you want to pursue. Once you decide, they can help you put a plan together based on the facts at hand. They’ll use their expert knowledge to work toward the resolution you want and make whatever modifications in the strategy necessary to try and achieve that outcome.

Similarly, our job as a trusted real estate professional, is to give you the best advice for your situation. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. We can’t because it’s impossible to know exactly what’s going to happen throughout your transaction. We also can’t predict exactly what will happen with conditions in today’s housing market.

But we, as expert real estate advisors, are knowledgeable about market trends and the ins and outs of the home buying and selling process. With that knowledge, we can anticipate what could happen based on your situation and help you put together a solid plan. We’ll also guide you through the process, helping you make decisions along the way.

That’s the very definition of getting the best – not perfect – advice. And that’s the power...and advantage of working with an expert real estate advisor from Braceland Homes.

Bottom Line

If you want trustworthy advice when buying or selling a home, call or text Braceland Homes today at 619-947-3560, so you have an expert real estate advisor on your side.

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession. However, an economic slowdown doesn’t necessarily mean homes will lose value. Normally that's not the case at a all.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

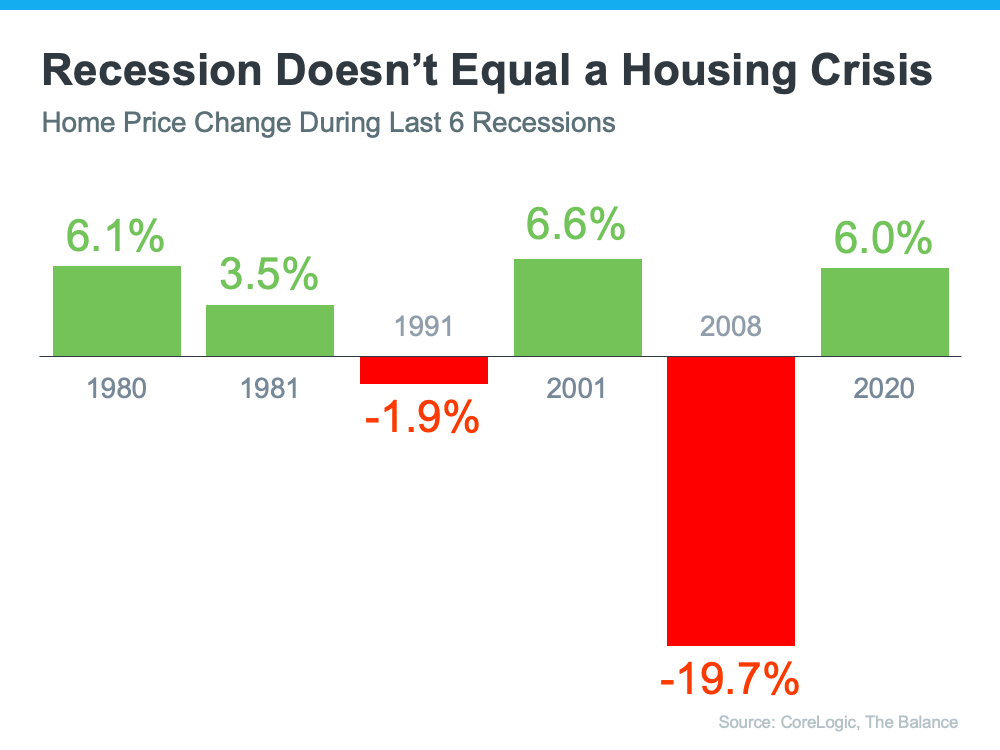

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

Bottom Line

We’re not currently in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

When you rent, you build your landlord’s wealth, your monthly payment depends on ever-rising rents, and you don’t benefit from home price appreciation.

On the other hand, when you own your home, you build your own wealth, and your monthly payment is locked in. It's essentially a super-charged savings account!

Finally, and this might just be the best reason, you benefit directly from home price appreciation. As the market rises, your home value goes up with it...without you doing anything at all!

If you’re feeling the challenges of a competitive market, remember that homeownership is a long-term game. Persevering today will lead to financial rewards in the future. The sooner you get started, the sooner you will benefit from the many reasons to own a home. Call us today at Braceland Homes so we can set you up for success 619-947-3560.

In today’s housing market, you home owners have a great opportunity to sell your house and receive the best terms for your personal situation. That’s because there’s a limited number of homes for sale, which is creating competition among buyers. Right now, home buyers want three things:

These home buyer needs give you, the home seller, an amazing advantage – also known as leverage – when you sell you sell your home.

What Does This Mean for Home Sellers Today?

You might already realize this enables you to sell at a good price, but you’re also in a great position to get the best terms to suit your needs.

According to the latest Realtors Confidence Index from the National Association of Realtors (NAR), the average home sold is receiving 4.8 offers. That’s why there’s a good chance you’ll get offers from multiple buyers who are willing to compete for your house. When you do, you should look closely at the terms of each offer to find out which one has the best options for you.

And if you have questions at any point in the process, remember we're just a phone call away, here at Braceland Homes. Call us at your convenience 619-947-3560. We are real estate professionals who understand the fine print, know how to compare the terms of various offers, and will help you select the best one for your situation.

Bottom Line

If you’re thinking of selling your home, know buyer demand in today’s market gives you a great opportunity to get the best terms and price when you sell your house. Call us today at 619-947-3560 today to discuss how much leverage you have as a seller in today’s market.

Is the housing market going to crash? What's next with home prices, the appreciation of homes, and housing affordability? All will be revealed, right now!

Welcome back to another real estate market update! I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here is where I share the latest news related to buying and selling residential real estate.

Now, first question, housing crash coming? Housing bubble? I'm not going to leave you in suspense. No and no. I know. You literally can't turn on the news, or look on the internet, and not see or hear something about a housing bubble or the impending housing market crash. I recently posted on the Braceland Homes blog about this with a post titled, “Two BIG Reasons Why We Are NOT in a Housing Bubble.”

That blog post centered around this graphic right here. This shows home values going all the way back to World War II. The reason we go back to World War II is, that was the start of the modern-day housing boom here in this country. When service members came back from the war, the GI Bill provided for education, and affordable home loans, so they could go out and buy a home. Ever since then, there’s only been one time in this country, where homes lost significant value. And that was back in 2008.

Back in 2008 we saw homes lose value mainly for two reasons. First reason was loose lending standards. You could qualify for a home with no income, no job, and no verification...and we know how that ended up. The second reason homes lost value during the housing crash was because of cash out refinances. People took the equity they had, cashed it out, bought jet ski, boats, RV and went on expensive vacations, financed through their homes. They did this thinking the exploding home appreciation would never end. But we now know it ended poorly. So let’s recap what happened there. Folks that couldn't afford homes in the first place, applied for loans they didn't have to qualify for, and then they took the equity from those homes, cashed it out and spend it. That’s essentially how we ended up with the housing crash in 2008.

So back in 2008, loose lending standards really drove the housing crisis. Today the bottom line is, lending standards are nothing like they were in the early 2000s. There’s two components that this report by the urban institute outlines. The red area there, product risk, or the mortgage industry. You'll see that's now, since 2008, been virtually eliminated through regulation. The brown portion is borrower risk. Think about that as asset profile, credit score, all the things it takes to qualify for a loan, and those also have been severely reduced through stricter standards. It’s gotten harder to qualify for a loan since the housing crisis. This graphic tells the story of the differences today between back then.

If you need further proof of how this is playing out in the housing market, just take a look here at foreclosure activity since 2005. The foreclosure market in this country is at an all-time low. To be perfectly transparent, there’s been a moratorium on foreclosures in place since the pandemic started. The federal government stepped in and said "we’re not going to process these foreclosures during the pandemic". And while we certainly don’t want to see anybody go through that, we will see a small number of foreclosures once the government lifts the moratorium, but nothing like the numbers we saw from 2007 through 2015, where there were over one million foreclosures per year.

You can also look at the loans that have been given to people with a credit score less than 620. Very few in comparison to the years leading up to the housing crash. So we can clearly say lending standards are different, and one of the major contributors of the crash back in 2008 is no longer around.

So the housing market isn't going to crash, and we're not in a housing bubble. That's good, but what lies ahead for us in the real estate realm? What does the rest of this year have in store? The Fed started off the month by raising the Fed funds rate. A lot of questions about that, as well as talks of a recession down the road. Home prices are going up. Interest rates are going up. So, a lot of questions about what’s ahead. Let me give you some perspective.

The most recent, updated, home price forecast, from seven of the leading industry forecasters, average 9% home price appreciation across the board right now for 2022. You may hear people, and even the media, saying that homes are going to lose value later in the year, but that's certainly not what the experts are saying.

If we look beyond this year, at this home price expectations survey, for the first quarter of this year, they’re again calling for 9% appreciation this year. We see alignment here, for this year, with the average from the forecasters illustrated on the last graphic. And then beyond this year, we move into what I’m going to call, a much more normal rate of home price appreciation. Before the pandemic, the average home price appreciation was about 3.8% in this country. And you see things returning to those levels for the next four years, after this year. Anybody wondering, is this the top of the market? Should I buy right now? These forecasts for home price appreciation going forward, may help you in making a powerful and confident decision on what to do next in regard to buying or selling your next home.

Now I want to quickly take a look at housing affordability. I know home prices seem completely out of control, right? And we can see right now that housing affordability is really approaching more historical levels. If you're new here, this is the Housing Affordability Index. It goes all the way back to 1990. And if you follow me, you’ve definitely seen this before. Anyway, with this index, the higher the bar, the more affordable homes are. If you look closely here, you'll see it's not so much that homes have been a really great value over the last decade or so. Homes now are not as affordable as they were over the past 10 or 12 years, and certainly not as affordable as they were in those orange bars, which was during the housing crisis. That’s when distressed properties dominated the market. Homes were being sold at a massive discount. We’re certainly not there. And as we’ve seen prices rise, and mortgage rates rise, homes are not as affordable as they were even over the past couple of years.

It’s important to remember that housing affordability is really a measure of three key things. I mentioned home prices and mortgage rates, but it’s also wages. Right now, all three of those things are ticking up, but historically, over the past couple of years, mortgage rates have kind of offset some of the rising prices. We’re no Longer sitting in that seat, so people are now feeling affordability challenges. It is important to keep this in context, and remain positive. Even though homes are less affordable now than the last decade or so, they are still MORE affordable than the two decades leading up to the housing crash! People are making better wages, and mortgage rates, although they are on the rise, are still lower than any time prior to the housing crash!

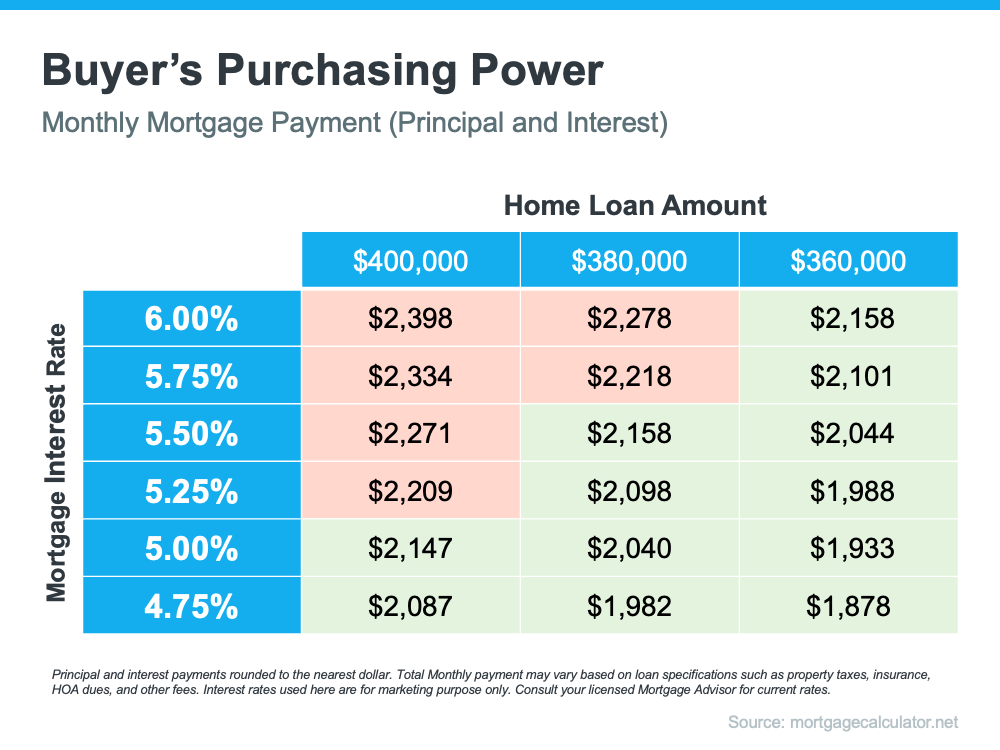

If you’re planning to buy a home, it’s critical to understand the relationship between mortgage rates and your purchasing power. Purchasing power is the amount of home you can afford to buy that’s within your financial reach. Mortgage rates directly impact the monthly payment you’ll have on the home you purchase. So, when rates rise, so does the monthly payment you’re able to lock in on your home loan. In a rising-rate environment like we’re in today, that could limit your future purchasing power.

Today, the average 30-year fixed mortgage rate is above 5%, and in the near term, experts say that’ll likely go up in the months ahead. You have the opportunity to get ahead of that increase if you buy now before that impacts your purchasing power.

Mortgage Rates Play a Large Role in Your Home Search

The chart below can help you understand the general relationship between mortgage rates and a typical monthly mortgage payment within a range of loan amounts. Let’s say your budget allows for a monthly mortgage payment in the $2,100-$2,200 range. The green in the chart indicates a payment within that range, while the red is a payment that exceeds it (see chart below):

As the chart shows, you’re more likely to exceed your target payment range as mortgage rates increase unless you pursue a lower home loan amount. If you’re ready to buy a home, use this as your motivation to purchase now, and call or text us at Braceland Homes 619-947-3560, so you can get ahead of rising rates before you have to make the decision to decrease what you borrow in order to stay comfortably within your budget.

Work with Trusted Advisors To Know Your Budget and Make a Plan

It’s critical to keep your budget top of mind as you’re searching for a home. Danielle Hale, Chief Economist at realtor.com, puts it best, advising that buyers should:

“Get preapproved with where rates are today, but also consider what would happen if rates were to go up, say another quarter of a point, . . . Know what that would do to your monthly costs and how comfortable you are with that, so that if rates do move higher, you already know how you need to adjust in response.”

No matter what, the best strategy is to work with us at Braceland Homes, and one of our trusted lenders, to create a plan that takes rising mortgage rates into consideration. Together, you can look at your budget based on where rates are today and craft a strategy so you’re ready to adjust as rates change.

Bottom Line

Even small increases in mortgage rates can impact your purchasing power. If you’re in the process of buying a home, it’s more important than ever to have a strong plan. Let’s connect so you have a trusted real estate advisor and a lender on your side who can help you strategize to achieve your dream of homeownership this season.

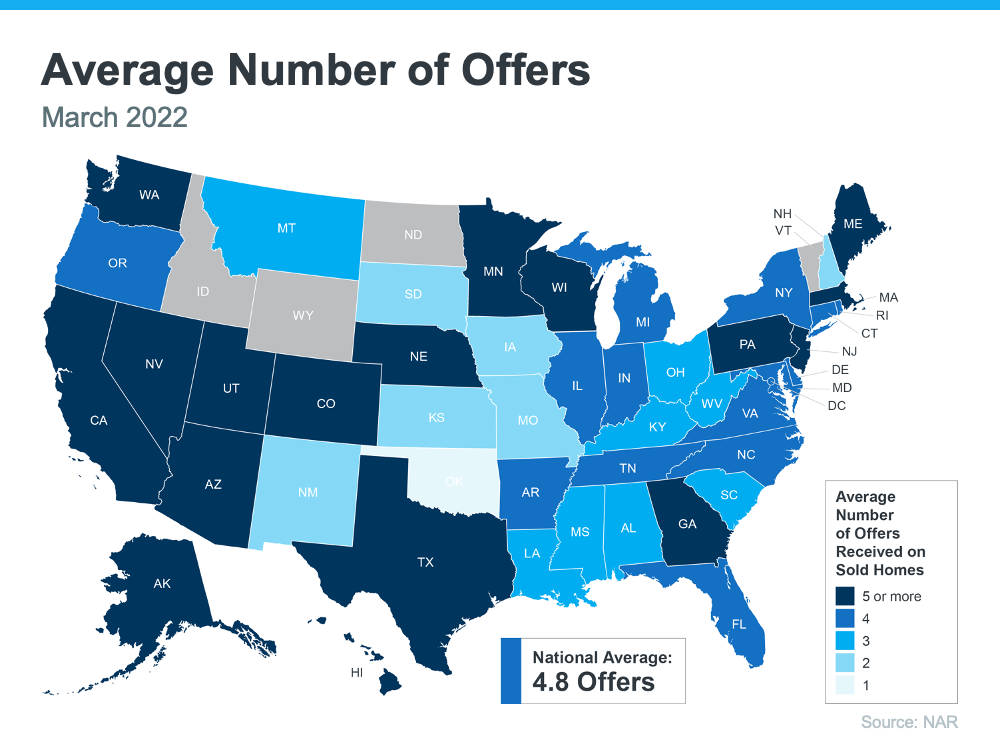

With a limited number of homes for sale today and so many buyers looking to make a purchase before mortgage rates rise further, bidding wars are common. According to the latest report from the National Association of Realtors (NAR), nationwide, homes are getting an average of 4.8 offers per sale. Here’s a look at how that breaks down state-by-state (see map below):

The same report from NAR shows the average buyer made two offers before getting their third offer accepted. In this type of competitive housing market, it’s important to know what levers you can pull to help you beat the competition. While a real estate professional is your ultimate guide to presenting a strong offer, here are a few things you could consider.

Offering over Asking Price

When you think of sweetening the deal for sellers, the first thought you likely have is around the price of the home. In today’s housing market, it’s true more homes are selling for over asking price because there are more buyers than there are homes for sale. You just want to make sure your offer is still within your budget and realistic for the market value in your area – that’s where my team and I at Braceland Homes can help you through the process. Bankrate says:

“Simply put, being willing to pay more money than other buyers is one of the best ways to get your offer accepted. You may not have to increase it by a lot — it’ll depend on the area and other factors — so look to your real estate agent for guidance.”

Putting Down a Bigger Earnest Money Deposit

You could also consider putting down a larger deposit up front. An earnest money deposit is a check you write to go along with your offer. If your offer is accepted, this deposit is credited toward your home purchase. NerdWallet explains how it works:

“A typical earnest money deposit is 1% to 2% of the home’s purchase price, but the amount varies by location. A higher earnest money deposit may catch a seller’s attention in a hot housing market.”

That’s because it shows the seller you’re seriously interested in their house and have already set aside money that you’re ready to put toward the purchase. We'll advise you on what's appropriate, and having the greatest success, in your area.

Making a Higher Down Payment

Another option is increasing how much of a down payment you’re going to make. The benefit of a higher down payment is you won’t have to finance as much. This helps the seller feel like there’s less risk of the deal or the financing falling through. You have more skin in the game, so to speak. And if other buyers put less down, it could be what helps your offer stand out from the crowd.

Non-Financial Options To Make a Strong Offer

Realtor.com points out that while increasing these financial portions of the deal can help, they’re not your only options:

“. . . Price is not the only factor sellers weigh when they look at offers. The buyer’s terms and contingencies are also taken into account, as well as pre-approval letters, appraisal requirements, and the closing time the buyer is asking for.”

When it’s time to make an offer, lean on us at Braceland Homes. We have insight into what sellers are looking for in your local market and can give you expert advice on what levers you may or may not want to pull when it’s time to write an offer.

From a non-financial perspective, this can include things like flexible move-in dates, or minimal contingencies (conditions you set that the seller must meet for the purchase to be finalized). For example, you could make an offer that’s not contingent on the sale of your current home. Just remember, there are certain contingencies you probably don’t want to forego, like your home inspection. Ultimately, the options you have can vary state-to-state, so it’s best to leverage me and my team for guidance.

Bottom Line

In today’s hot housing market, you need a partner who can serve as your guide, especially when it comes to making a strong offer. Give us a call at Braceland Homes 619-947-3560 so you have a trusted resource and coach on how to make the strongest offer possible for your specific situation.

Since the number of homes for sale is low today, it can feel challenging to find one that checks all your boxes. But if you know which features are absolutely essential in your next home and which ones are just nice bonuses, you can land a home that fits your needs.

Danielle Hale, Chief Economist for realtor.com, explains it like this:

“Focus on the goal you set out for yourself, like your list of must-haves and nice-to-haves and your budget, . . . Stick to that. Be persistent.”

So how do you go about creating your list of desired features? The first step is to get pre-approved for your mortgage. Pre-approval helps you better understand your budget, and that plays an important role in how you’ll craft your list. After all, you don’t want to fall in love with a home that’s too far out of reach.

Once you have a good grasp of your budget, you can begin to list all the features of a home you would like. Here’s a great way to think about them before you begin:

Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle (examples: distance from work or loved ones, number of bedrooms/bathrooms, etc.).

Nice-To-Haves – These are features that you’d love to have but can live without. Nice-To-Haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of the these, it’s a contender (examples: a second home office, garage, etc.).

DreamState– This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner (examples: farmhouse sink, multiple walk-in closets, etc.).

Finally, once you’ve created your list and categorized it in a way that works for you, discuss it with a real estate professional here at Braceland Homes. We’ll be able to help you refine the list further, coach you through the best way to stick to it, and find a home in your area that meets your needs. I coach my clients using the graphic above. I advise they choose just two or three of these five factors, depending on their budget, to really focus on. Unless you are blessed with an unlimited budget, it may be tough to get all five of these in a super hot, competitive market like the one here in San Diego.

Bottom Line

Crafting your home search checklist may seem like a small task, but it can save you time and money. It’s also one of the keys to being successful in today’s competitive market. Call us at Braceland Homes 619-947-3560, so we can work together to find a home that fits your wants and needs.

Buying a home and wondering if your inspection is necessary? While some buyers may decide to waive their inspection, it could be a risky decision.

Your home inspection is a crucial step in the homebuying process. It assesses the condition of the home you plan to purchase, so you can avoid costly surprises down the road.

Call or text us at Braceland Homes 619-947-3560 so you have expert advice and a trusted professional who will keep your interests top of mind, when the time is right.

Buying your first home is a major decision and an exciting milestone. Even though it can feel daunting at times, it has the power to change your life for the better. If you're looking to purchase your first home, you may be wondering what's happening in the housing market today, how much you need to save, and where to start.

Here are three things that can help give you the information you need to confidently pursue your dream of homeownership.

1. Consider All Options When the Number of Homes for Sale Is Low

Today, there are far more buyers in the market than there are homes available for sale. When that happens, it’s a good idea to do what you can to increase your pool of options. That could mean expanding your search to include additional housing types. For first-time buyers, considering condominiums (condos) and townhomes can be an excellent way to increase your choices. According to Bankrate:

“Townhomes often cost less than single-family homes of a similar size in the same location.”

In another article, they say:

“Buying a condo can be a great way to dive into homeownership without worrying about the upkeep that comes with single-family homes and townhouses.”

Condos and townhomes are both great entryways into homeownership. When you buy either one, you can start building equity which increases your net worth and can fuel a future move.

2. Know Your Down Payment Could Be More Within Reach Than You Think

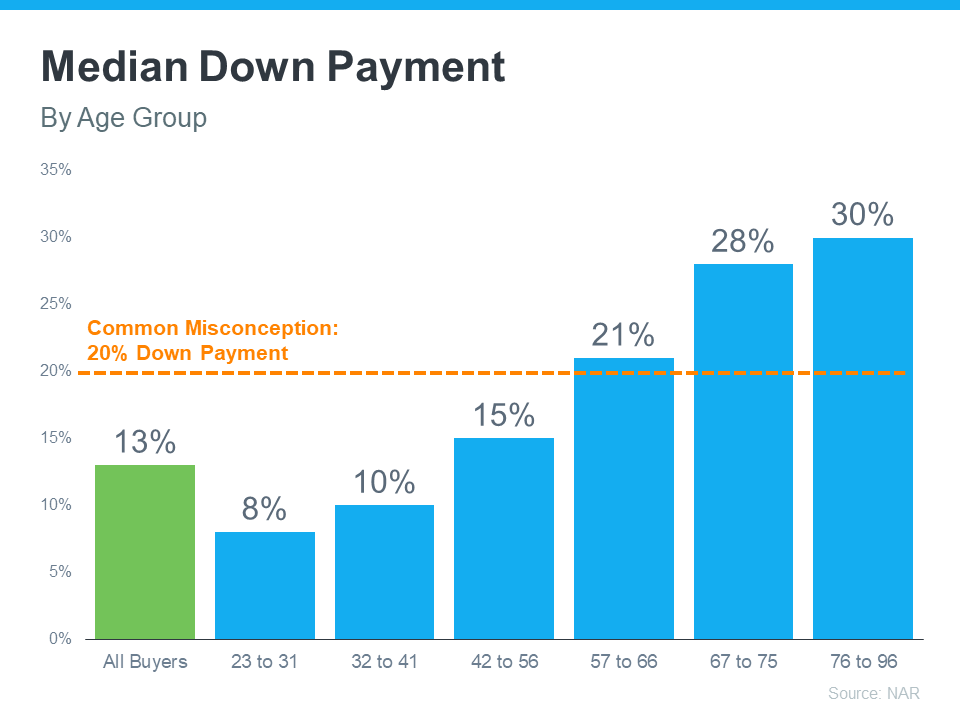

Saving for a down payment can feel like one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As the National Association of Realtors (NAR) says:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership.”

Data from NAR shows the median down payment hasn’t been over 20% since 2005. The graph below breaks down the median down payment by age group for recent homebuyers according to the 2022 Home Buyers and Sellers Generational Trends Report from NAR (see graph below):

Based on the data above, the median down payment for all homebuyers is only 13%. That’s well below the common misconception of 20%, and it’s even lower for younger buyers. This could mean you may not need to save as much for a down payment as you initially thought.

There are also down payment assistance programs available for many buyers. Not to mention, some loan options require as little as 3.5% (or even 0%) down for buyers who qualify. While there are advantages to putting 20% down, especially in today’s competitive market, know that you have options. To get more information on how much you may need to save and the help that’s available, talk with a professional.

3. Work with a Trusted Real Estate Advisor Throughout the Process

Finally, no matter where you’re at in your homeownership journey, the best way to make sure you’re set up for success is to let our team of professionals at Braceland Homes guide you in your home buying journey.

If you’re just starting out, we can help you with the initial steps, like educating you on the process and connecting you with a trusted lender to get pre-approved. Once you’re ready to begin your search, we can help you understand the local market and search for available homes. And when it’s time to make an offer, we’ll be that expert advisor and negotiator to help your offer stand out above all the rest.

Bottom Line

Knowledge is key to succeeding on your home buying journey. Knowing market trends, what you need for a down payment, and what options you have as a buyer today can give you the confidence you need to successfully buy a home. Give us a call at Braceland Homes today 619-947-3560 so you have an expert on your side who can help you navigate the home buying process.

Even if you haven’t been following real estate news, you’ve likely heard about the current sellers’ market. That’s because there’s a lot of talk about how strong market conditions are for people who want to sell their houses. But if you’re thinking about listing your house, you probably want to know: what does being in a sellers’ market really mean?

What Is a Sellers’ Market?

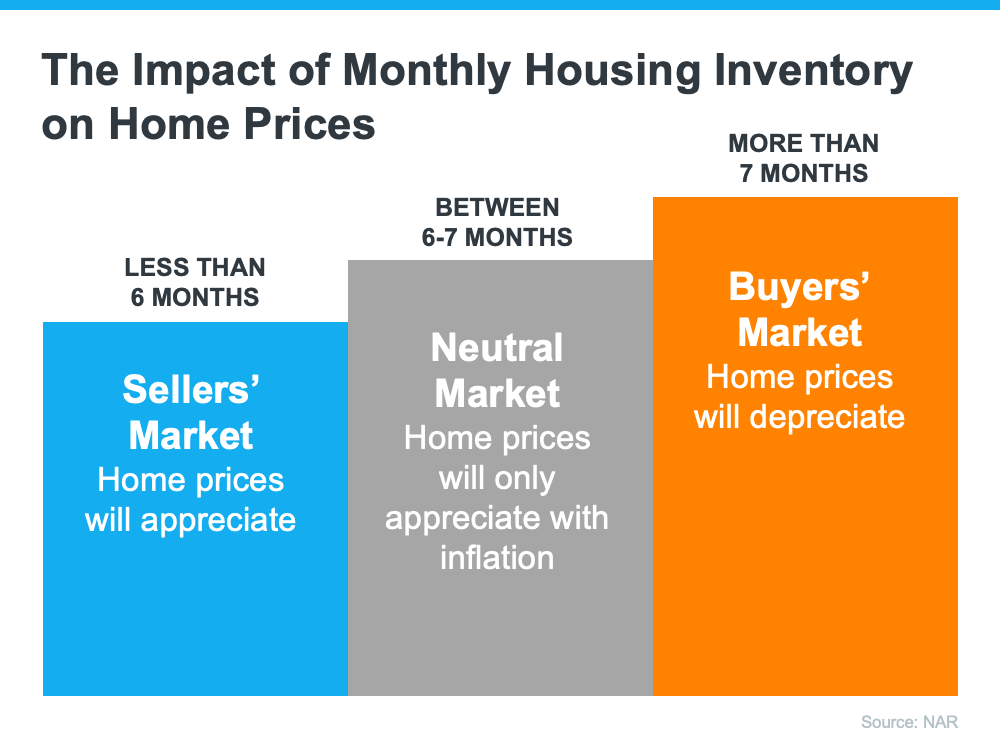

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still very low. There’s a 2-month supply of homes at the current sales pace.

Historically, a 6-month supply is necessary for a normal or neutral market where there are enough homes available for active buyers. That puts today, deep in sellers’ market territory (see graph below):

What Does This Mean for You When You Sell?

When the supply of houses for sale is as low as it is right now, it’s much harder for home buyers to find homes to purchase. That creates increased competition among home purchasers which can lead to more bidding wars. And if home buyers know they may be entering a bidding war, they’re going to do their best to submit a very attractive offer upfront. This could drive the final price of your house up.

And because mortgage rates and home prices are also climbing, serious home buyers are motivated to make their purchase soon, before those two things rise even further. That means, if you put your house on the market while supply is still low, it will likely get a lot of attention from competitive buyers.

Bottom Line

The current real estate market has incredible opportunities for home owners looking to make a move. Listing your house now means you’ll be in front of serious buyers who are ready to buy. Give us a call today at 619-947-3560 so you can jumpstart the selling process.