Braceland Homes Inc. is an Escondido, CA real estate brokerage founded in 2018 by retired US Navy officer Erik Braceland (DRE 02059069). Erik launched his second career after several underwhelming experiences with REALTORS® he worked with to buy and sell his own investment properties while serving on active duty. His systems, processes, and strategies positively impact the way homes are sold, and the systematic trademarked approach he embraces, guarantees his clients' satisfaction and success.

The link between financial security and homeownership is especially important today as inflation rises. But many people may not realize just how much owning a home contributes to your overall net worth. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

"Homeownership is rewarding in so many ways and can serve as a vital component in achieving financial stability."

Here are just a few reasons why, if you’re looking to increase your financial stability, homeownership is a worthwhile goal.

Owning a Home Is a Building Block for Financial Success

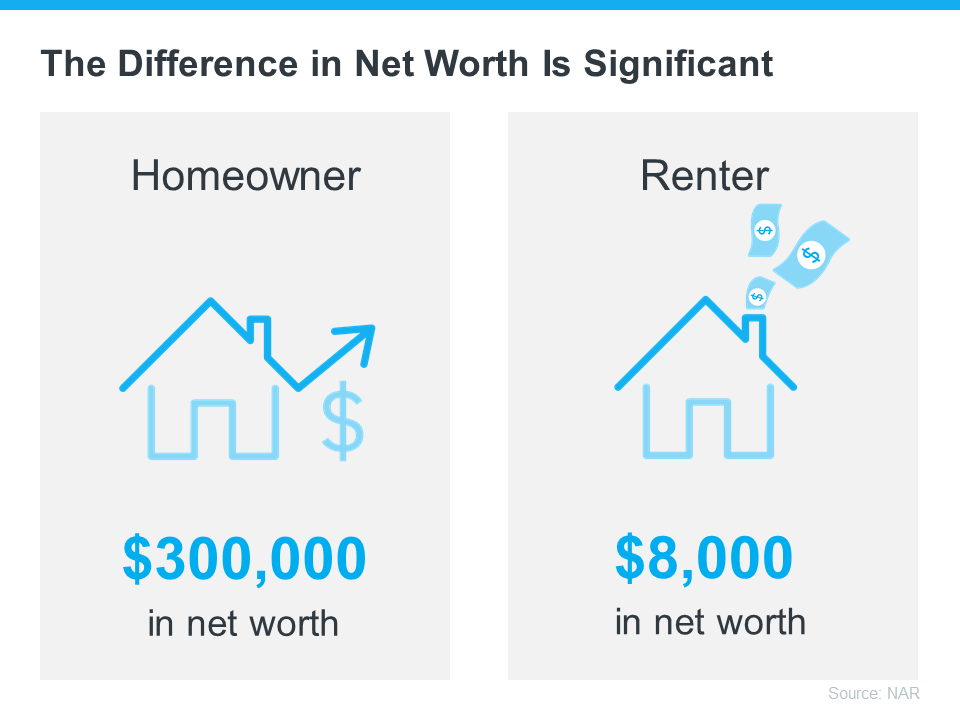

A recent NAR report details several homeownership trends and statistics, including the difference in net worth between homeowners and renters. It finds:

“. . . the net worth of a homeowner was about $300,000 while that of a renter’s was $8,000 in 2021.”

To put that into perspective, the average homeowner’s net worth is roughly 40 times that of a renter(see visual below):

The results from this report show that owning a home is a key piece to the puzzle when building your overall net worth.

Equity Gains Can Substantially Boost a Homeowner’s Net Worth

The net worth gap between owners and renters exists in large part because homeowners build equity. As a homeowner, your equity grows as your home appreciates in value and you make your mortgage payments each month.

In other words, when you own your home, you have the benefit of your mortgage payment acting as a contribution to a forced savings account. And when you sell, any equity you’ve built up comes back to you. As a renter, you’ll never see a return on the money you pay out in rent every month.

To sum it up, NAR says it simply:

“Homeownership has always been an important way to build wealth.”

Bottom Line

The gap between a homeowner’s net worth and a renter’s shows how truly foundational homeownership is to wealth-building. If you’re ready to start on your journey to homeownership, give us a call at Braceland Homes 619-947-3560.

For the first time in a long time, the number of newly listed homes has been rising throughout the year...as I predicted back in December of last year. Check out my prediction here:

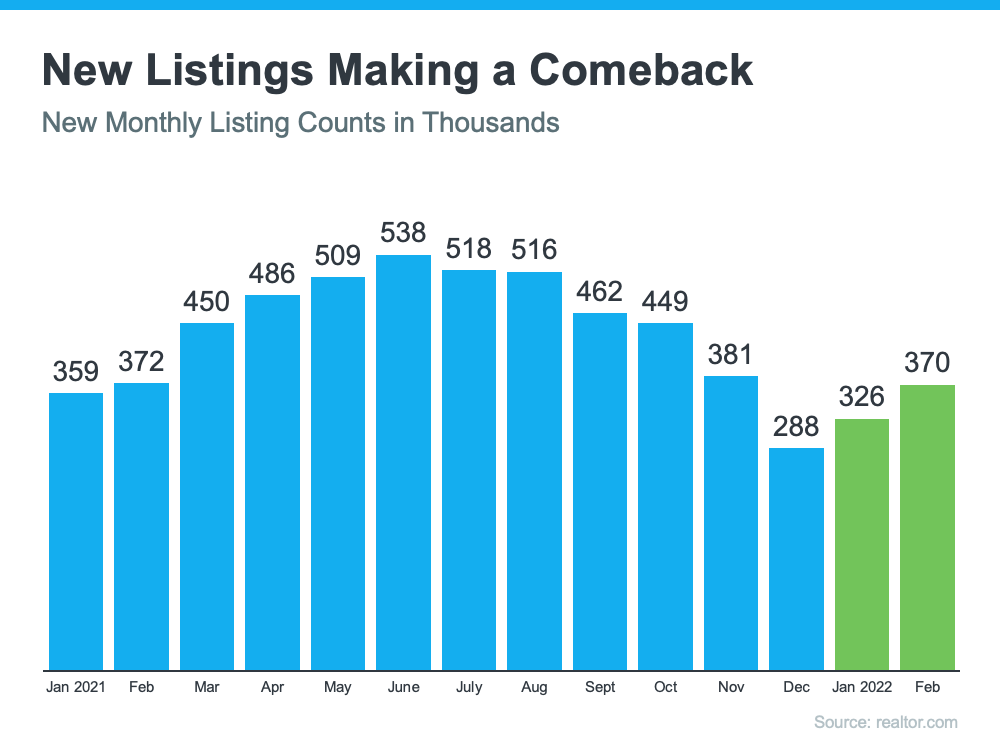

In their latest monthly release, realtor.com reveals the number of existing homes entering the market has increased for two months in a row (this comes after six months of declines). Here’s a graph showing the monthly new listings going back to January of last year. The green bars indicate the first gains since June.

However, buying demand is still outpacing housing supply.

Though the increase in homes coming to the market is great news for prospective homebuyers, the number of buyers is still outpacing the number of homes available for sale. As realtor.com explains in their latest report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

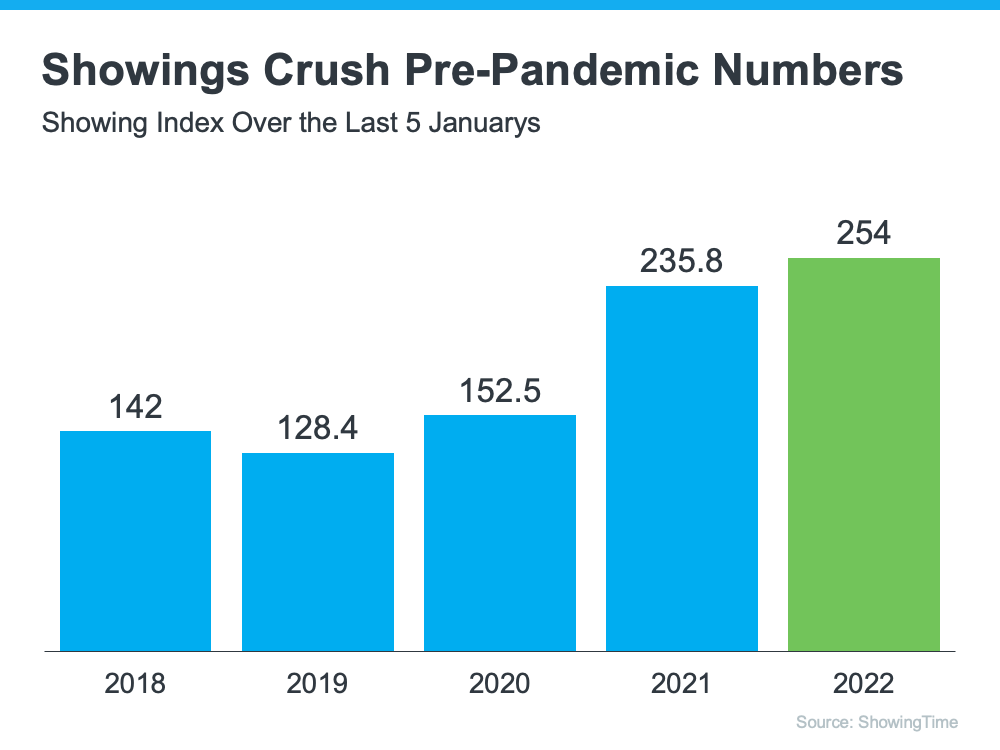

In fact, according to the latest ShowingTime Showing Index, which tracks the average number of appointments received on active listings during the month, buyer demand was greater this January than any other January in the last five years (see graph below):

This prompted ShowingTime to say:

“The latest data from ShowingTime . . . shows a surge in home buyer demand in January. . . . This enormous activity occurred in a month when buyer activity typically slows and followed a historic 2021, where buyer demand across the country was extraordinarily strong.”

What does that mean for you?

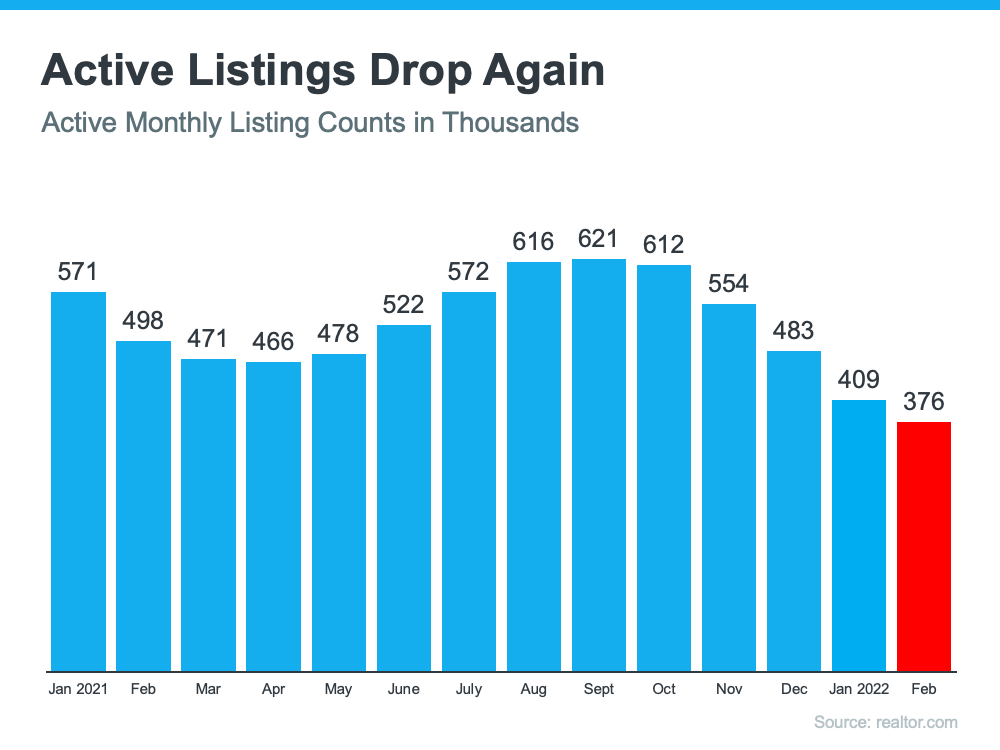

Basically, as homes come to the market, they are quickly being purchased by eagerly awaiting buyers. So even though the number of newly listed homes is increasing, the number of active listings is still shrinking every month because buyers are purchasing homes almost as soon as they come up for sale. That means listings are coming on and off the market so fast that they don’t carry over to be counted in the active listing numbers the following month. Here’s a graph showing the number of active listings each month since last January using data released by realtor.com:

This graph shows that the number of active listings has decreased for each of the last five months even though the number of newly listed homes has increased over the last two months.

Bottom Line

Whether you’re looking to upgrade to a home that will better suit your lifestyle or looking to purchase your first house, give us a call at Braceland Homes 619-947-3560 so you can stay updated on what’s happening in your area. And be prepared to move immediately if a home fitting your needs hits the market. Your dream home may be one of those new listings that just became available, but if you don’t act quickly, it could be gone tomorrow.

If you’re thinking of buying a home today, you already know that the number of homes available for sale is low. But what does that really mean for you? As a buyer, low housing supply coupled with high buyer demand means you should be prepared to navigate a highly competitive market where homes sell fast and get multiple offers. Realtor.com has this to say:

“Homes also flew off the market at record pace as buyers put offers in the moment properties came up for sale….”

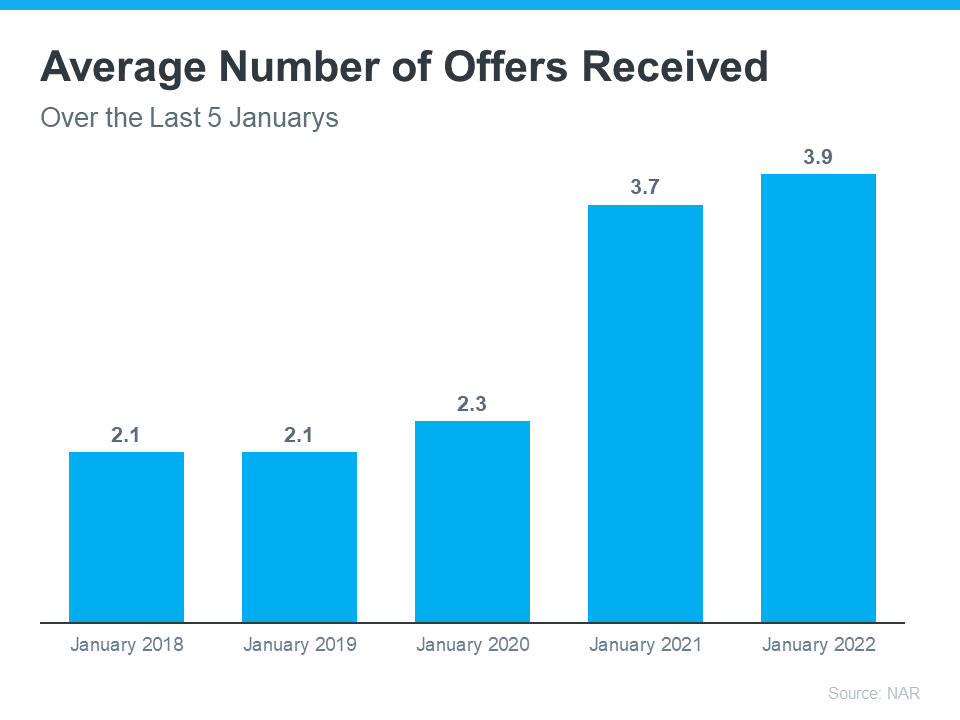

In a bidding war situation like this, doing everything you can to get ahead of the competition is a wise move. That’s because when you find a house and submit an offer, it’ll likely be up against strong offers from other buyers. According to the latest RealtorsConfidence Index from the National Association of Realtors (NAR), homes today are receiving an average of 3.9 offers. That’s the most offers we’ve seen in January for the last 5 years (see graph below):

To help you navigate bidding wars with multiple offers, an expert real estate advisor is key. At Braceland Homes, we know what’s worked for other buyers, what sellers are looking for, and how to help you prepare when it comes time to make an offer. Here are three tips to keep in mind that will help you make the best offer possible.

1. Know Your Numbers

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with one of our lenders so you can get pre-approved for a loan. Pre-approval shows sellers you’re serious, which can give you a competitive edge. You should also know making an offer at the home’s asking price may not be enough. Homes today often sell for more than their listing price. Here in our San Diego housing market that can typically be an extra 5%. We can help you understand the market value of the home and what other homes are selling for in your area.

2. Be Ready To Move Fast

Speed and the pace of sales are contributing factors to today’s competitive housing market. When homes are selling fast, it’s important to stay on top of the market and be ready to move quickly. We will help you stay up to date on the latest listings and help you put together your best offer as soon as you find the home you want to buy.

3. Make a Strong but Fair Offer

When you’re up against other offers, putting your best offer forward from the start is key. Lean on us at Braceland Homes to write a strong offer and use our expertise on which levers you can pull to make your offer as enticing as possible. One option is to wave some of your contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Just remember there are certain contingencies you don’t want to give up, like the home inspection.

Bottom Line

No matter what, Braceland Homes is your best resource for making an offer that stands out in a competitive market. Give us a call at 619-947-3560 to talk through what you can expect as a buyer and how to kick off a successful home search.

How is the conflict between the Ukraine and Russia affecting the housing market here in the US?

Welcome back to another real estate market update! I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes Blog we cover topics related to buying and selling residential real estate, and trends happening across the housing market, with new videos every Thursday.

We’ve talked a lot about home price appreciation in the past, and I’m sure you want to know where that's headed after our inflation talk last week. And as we think about rising prices in general. If you haven't already gotten it from my clever image here, home prices are projected to continue rising...believe it, or not.

Let’s take a look at this graph from the Home Price Expectation Survey. I think this gives you a real clear picture of where home prices are projected to go according to the leading experts in the field. Now the Home Price Expectation Survey is a survey of 100 economists. These are data analysts, people who are projecting out home price appreciation. And in the fourth quarter of last year, this is the projection for cumulative house appreciation by 2026. So, what are we looking at? They divided out the group into optimists and pessimists. Optimists being the ones projecting the most appreciation over the next five years, and pessimists estimating on the lower side. Take a look at that orange bar on the right. Those are the pessimists. The experts, that are considered pessimists, are saying that cumulative home price appreciation, by 2026, is going to be over 23 percent, on the low side. Pretty substantial even on the low side. The you can see the optimistic experts are projecting over 62% cumulative home price appreciation over the next five years on the high side. And finally, if we average the opinions of all these expert economists, we are looking at a gain of just over 43%.

So then, what’s projected to happen? Home values are expected to increase in value over time, as they normally do, but at a pretty significant rate over the next five years. Now This, is pretty important, to those of you thinking of making a move. Locking in today’s cost is mission critical for those of you who have the opportunity to do so. Check out this video, titled Hedge Against Inflation With Real Estate:

You want to protect yourselves from rising interest rates, that we'll talk about in just a minute, and rising prices, that are all around us, by locking in, or fixing, your largest monthly payment with a mortgage.

Now Let’s talk a little bit about mortgage interest rates. A lot of you are probably wondering about Russia and Ukraine, and how that tragic situation is going to affect things. So, let's take a look at where we are today, and then I'll keep you posted as we move forward, with fresh updates on what’s happening with these mortgage rates.

Right now we're seeing a bit of a reprieve with the rise in interest rates. Freddie Mac saying, “Geopolitical tensions caused U.S. Treasury yields to recede this week as investors moved to the safety of bonds, leading to a drop in mortgage rates. While inflationary pressures remain, the cascading impacts of the war in Ukraine have created market uncertainty. Consequently, rates are expected to stay low in the short-term but will likely increase in the coming months." So as of last week, looks like things have indeed cooled a bit from the peak of 3.92% in mid Feb. So, three take-aways here. First, they reference the treasury yield, because historically, interest rates tend to follow the trajectory of the 10-year treasury yield, so it’s a good indicator of how things will shake out. Second, there's market uncertainty because of the war. And third, rates are only expected to stay low for a short time. So, there is a window of opportunity here if you are planning to make a move. And as always, I want o present those opportunities to you whenever they appear.

We have a visual showing us the progression of mortgage rate going back to January of 2020. You can clearly see where rates dropped to a low of almost three percent in January of last year during the pandemic - another period of crisis, and opportunity – and then slowly rising up to almost four percent last month. And you see the roughly quarter point dip as the conflict with Russia and Ukraine really heated up.

Hear we have another quote from the National Association of Realtors saying something very similar to Freddie Mac, "Following the trend of the 10-year Treasury yield, mortgage rates will likely fall, remaining below 3.9% this week. However, expect mortgage rates to rise later this month as the Fed will raise interest rates." Again, they touch on the ten-year treasury yield I spoke about earlier and how it’s a great indicator of where mortgage rates will go, and they also emphasis that rates won't remain low. NAR also mentions the FED, which doesn't control mortgage rates, but does have influence over them.

The First American Financial Corporation echoes these previous sentiments with this, "The 10-year Treasury yield is down… likely in response to the worsening Russia-Ukraine conflict, and mortgage rates may follow suit."

Let's take a look at that 10-year Treasury yield here. You can see how it looks a lot like the right half of the graph we saw earlier showing mortgage rate changes, and why it might be such a good indicator of the that mortgage rate trajectory. Just like the mortgage rate graph, it starts low in January of last year, and then climbs through the beginning of February, finally dropping off in mid-February. But its already coming back up in March, so we may see that increase in mortgage rates resume any day.

I do want to put this in perspective for you, and this graphic does a great job of that. Even with mortgage interest rates rising, where we are today is still lower than where mortgage rates have been at any time over the last 50 years! Think about that. It's just really amazing! Look at the double-digit interest rates in the eighties!

Yes, home prices are nuts, but as I've demonstrated in the past, home prices and mortgage rates tend to rise together. If you have a move in your future, sooner really is better than later for so many reasons right now. Great low mortgage rates that are rising, and high home prices that are only getting higher are two of the big ones.

If you've enjoyed this content or found it helpful, please hit that like button. It really does mean a lot, and keeps me motivated to produce more free content. And please share this content with someone you think might benefit from it. Thanks for joining me, and I'll see you right back here soon!

The Difference Between Renting a Home and Owning a Home

If you’re deciding whether to rent or buy, consider the many financial benefits that come with owning a home. Also check out this video on the Amazing Non-Financial Benefits of Homeownership:

As a renter, you build your landlord’s wealth and face rising costs. As a homeowner, you build your own net worth and can lock in your monthly payments for the length of your loan. Check out my video on using real estate to hedge against inflation:

If you’re weighing your options, remember that owning a home is a decision that has considerable financial perks. If you want to learn more, give me a call at Braceland Homes 619-947-3560, to talk about the perks of homeownership.

Today I'm going to tell you about what I believe to be, the best hedge against inflation, and the best way that you can protect yourselves from the current rising costs of everything.

Welcome back to another real estate market update! I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes Blog we cover topics related to buying and selling residential real estate, and trends happening across the housing market. Please consider subscribing to our channel so you can be updated and ready to go with all the latest knowledge headed into each weekend.

Prices are going up on everything, and as we see prices rise around us at the gas pump, the grocery store, and the car dealership, we also know that homeownership costs are certainly not immune to that in any way, nor are home rental rates. And I want you home buyers out there to really pay special attention to this episode. We'll talk about rising rent in a bit, but one of the things I really want to focus on, is how locking in your fixed monthly housing cost, probably the biggest cost that you have...and locking that housing cost in at today’s price, and why it's so beneficial to safeguarding you against that inflation and those rising costs all around us. We want to hedge against inflation, with real estate.

I want to help you understand how to beat inflation. We'll begin with a quote from Investopedia. It says, “Real estate is one of the time-honored inflation hedges. It’s a tangible asset and those tend to hold their value when inflation reigns, unlike paper assets. More specifically, as prices rise so do property values.” What we can see here is that homeownership is one of those costs or expenses that you can lock in today. It’s an asset that’s increasing in value over time. And as prices rise, and home values rise, and prices on everything else rise around us...locking in that one, really large, fixed expense of housing is really a game-changing hedge against inflation tomorrow.

This visual shows how homeownership outperforms inflation over time. This is homeownership as a hedge against inflation, and I want to break it down for you so you can really see what we’re talking about here. This is home price appreciation versus the consumer price increases over time, and it goes all the way back to the 1970s. Now the blue bars are the average inflation rate for the decade, and the green bars are the average home price appreciation for each of those decades. Let’s look at the 1970s to start. Inflation increased at 7.1 percent in that decade, and home values appreciated at 9.9 percent in that same time period. So, homeownership outperformed inflation. And where do you want to be in inflationary times? In an asset that’s outperforming inflation! Now in the 1980s it was a little bit more balanced with 5.6 percent inflation, and 5.5 percent home price appreciation. Look at the ‘90s. We start to see home values rise again a little bit more, outperforming inflation throughout that decade. Now you probably know the 2000s were very different. Home prices performed at a very different rate than what we’ve seen in many other decades, and even what we’re seeing today, and potentially tomorrow. We also had a fundamentally different housing market. We had the oversupply of homes, and lending standards that were vastly different than they are today. Homeowners also didn’t have the equity that they have in their homes right now. A fundamentally different housing market, where home prices did not outperform inflation in the 2000s. But look at the 2010s. This is where home values really started to kick in. Homes started appreciating much faster than inflation. 4.9 percent versus 1.8. And then 2020 and 2021, you know what’s happened with the housing market here; massive home price appreciation! A drastic difference here, where home values outperformed inflation.

So over time what you can see, is that you can hedge against inflation with real estate, because the rise in home values, generally outperforms the rate of inflation. That means that if you buy a home today, you can lock in today’s cost, and hedge against inflation with your new real estate and fixed mortgage rate. In this scenario, your housing costs are now fixed for the term of the loan, probably the next 30 years. Now, this becomes really important when we start to talk about renting, because renting takes on the risk of rising rental prices year after year after year. I’ve shown you that data in the past, if you’ve been following along with me. Rental prices are truly skyrocketing. Would you rather assume 30 years of price increases, or pay the same monthly payment for the next 30 years? Seems like a really simple question to answer. Now I know there are special circumstances why someone might take the former over the latter, but for me, I'll take the security of that fixed payment every time! Set it...and For Get It! Anyway, if you are enjoying these insights so far, please let me know in the comments below.

So, let me share a quote with you here, from Bankrate, that’s really powerful for renters. It says “A fixed rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.” That’s certainly not the case if you’re renting, and that’s because rental prices rise year after year. This becomes really powerful for some of you that might be thinking "I could buy today, but I’m just gonna press pause, and I’m going to wait. I’m going to wait and see what happens to home values. I'll wait to see if they drop, or if they rise." Well, all the forecasts that we’ve seen show that home values are projected to continue rising.

We also know that mortgage rates are projected to keep rising, and we know that rental prices are rising. What does that mean at the end of the day? Two things really. One, someone who continues to rent, but could buy, is taking on the additional increases in rent year after year. Two, it’s going to cost more to buy a home down the road. So really important for you renters to understand this dynamic, and I think this next visual really helps show how rental prices compare to inflation rate.

This shows that rent increase has been greater than inflation in most years, so let me break it down again. Rental price appreciation versus core inflation rate, again, going all the way back to the ‘70s. So your blue line is that core inflation rate, and your green line is rental price appreciation, and what do we see on a whole? The green line higher than the blue line in most scenarios, meaning that rental prices have increased at a faster rate than inflation in most times. Yes, there’s some ticks down below that blue line; however, that means it’s more expensive to rent over time because rental prices are continuing to rise faster than the rate of inflation. So no pressure, but you really do want to buy a home now, if at all possible, to avoid those increasing costs for rent and inflation all around us.

So, is real estate a good hedge against inflation? I think this really kind of brings it home for us. This is from Forbes, - it says, “Homeowners are shielded from mounting rental prices because their cost is fixed, regardless of what’s happening in the housing market." Like we talked about, you’re locking in that payment at today’s cost. They go on to say, "Tangible assets like real estate get more valuable over time", and you’ve seen that in the graphs and the data that I’ve shown you, "which makes buying a home a good way to spend your money during inflationary times." Well said.

I really wanted to write this now, because I realize we're all struggling with the prices of everything spiraling out of control, and I know that this is one way to take some of that control back, over probably the largest monthly payment that most of us have to make. I hope you found this helpful. Please let me know what you think of this strategy to combat inflation. Do you also believe that real estate is a great hedge against inflation? And do you have any other ideas on how to beat inflation? Please share with the group in the comments below so we can all learn from each other, and make the most of our current circumstances.

If you've enjoyed this content or found it helpful, please share this it...so more people can benefit from it.

That's all for now. I'm Erik Braceland, and thanks once again for stopping by the Braceland Homes Blog. Thank you for increasing your financial literacy and considering real estate as a way to make things happen for you and your family. I'll see you right back here real soon!

![The Difference Between Renting and Owning [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/02/24130106/20220225-MEM-1046x2279.png)