Braceland Homes Inc. is an Escondido, CA real estate brokerage founded in 2018 by retired US Navy officer Erik Braceland (DRE 02059069). Erik launched his second career after several underwhelming experiences with REALTORS® he worked with to buy and sell his own investment properties while serving on active duty. His systems, processes, and strategies positively impact the way homes are sold, and the systematic trademarked approach he embraces, guarantees his clients' satisfaction and success.

Financial benefits are always a key aspect of homeownership, but it’s also important to understand that the non-financial benefits of homeownership are why so many people genuinely fall in love with their homes. When you own your home, you likely feel a sense of emotional attachment because of the comfort it provides, but also because it’s a space that’s truly yours.

Over the past two years, we’ve learned to love our homes even more as we’ve stayed home more than ever due to the ongoing pandemic. As a result, the personal and emotional benefits our homes provide have become even more important to us.

As the most recent State of the American Homeowner from Unison puts it:

“Despite the upheaval and uncertainty of the past year, one thing has stayed the same: the home continues to be of the utmost importance and a place of security and comfort.”

When the health crisis began, the world around us changed almost overnight, and our homes were redefined. Our needs shifted, and our shelters became a place that protected us on a whole new level. The same study from Unison notes:

91% of homeowners say they feel secure, stable, or successful owning a home

64% of American homeowners say living through a pandemic has made their home more important to them than ever

83% of homeowners say their home has kept them safe during the COVID-19 pandemic

It’s no surprise this study also reveals that homeowners now love their homes even more as our emotional attachments to them have grown:

That sense of emotional connection genuinely reaches far beyond the financial aspect of homeownership. Because they’re our shelters – ones that we can genuinely call our own. Our homes touch our hearts and can also positively impact our mental health.

As JD Esajian, President of CT Homes, LLC, says:

“Aside from the financial factors, there are several social benefits of homeownership and stable housing to consider. It has long been thought that buying a home contributes to a sense of accomplishment. Still, most individuals fail to realize that homeownership can benefit your mental health and the community around you.”

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, take a moment to reflect on what Mark Fleming, Chief Economist at First American, notes:

“Buying a home is not just a financial decision. It’s also a lifestyle decision.”

For more on the non-financial benefits of homeownership, check this recent video from Braceland Homes on the subject:

Bottom Line

There are so many reasons to fall head over heels for homeownership. Your home will provide a place to customize and call your own, in addition to stability and security. If you’re ready to fall in love with homeownership, give us a call at Braceland Homes 619-947-3560 so you can get started on your home buying journey today.

This Year's Biggest Real Estate Opportunity For Home Owners

Where is today's big real estate opportunity? It’s right here. It is in your home equity!

Welcome back to another real estate market update! I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home.

Today I’m going to break down the current situation with home equity, kind of wrapping up this past year. I'll show you the latest, very impressive, numbers we have from this past year.

I really think this is the current real estate opportunity. It may be driving a lot of you prospective home buyers. "Do we harness that home equity and move up? Maybe if we’re retiring, we downsize, and use all that accumulated home equity and home sale profit to build a little bit of a nest egg." A number of different things that people are doing with home equity right now. It definitely there in abundance. And a lot of you are thinking, and actively considering using that home equity to do something different with your housing situation. Let us know what you're thinking of doing in the comments below!

So how to calculate home equity? It’s a pretty simple equation once you have two main data points. Do you know how much you owe on your home? Do you know how much your home is worth? Those two bits of information give you the equity. You just subtract what you owe from what your home is worth. And yes, I'm available to help you with the second piece. Just contact me at 619-947-3560. You can get a ball park idea of what your home can sell for online. But I can give you a much more accurate value by taking a look at your home in person, and accounting for the home's current condition, as well as all you've done...or haven’t done, to your home. Anyway, that's how you find equity on a house.

CoreLogic’s third quarter home equity report showed that the average homeowner with a mortgage gained $57,000 in equity across the nation. Boom. We could wrap up right here. What an awesome gain! $57,000 as of the third quarter 2021 for home equity. Those are the latest numbers we have. The average growth in equity in a home. But don't leave just yet. I have more for you. There’s so many of you that tune in from many different parts of the country to our weekly housing market updates, and I know you're wondering, "what about where I'm at?". Fifty-seven thousand is the average, so let's call that somewhere other than on the coast. Here on the West Coast or here in the San Diego housing market it’s more in the neighborhood of twice that much. If you’re in the middle of the country maybe it’s that fifty-seven thousand. Maybe it’s a little bit more, depending on where you are. But $57,000 last year. That’s a shocking number to many of us, right? Perhaps we need to put that to work for us somehow. 31.1% is the year over year percentage for increase in equity in the U.S., for homes with mortgages. $3.2 trillion is the rise in equity. They go on to say "this summer, home price growth reached its highest level in more than 45 years, pushing equity gains to another record high". So, equity, is clearly the shining star of the pandemic. You know, the story continues on. We talked about the pandemic in 2020, how home equity was keeping people out of trouble because they could tap into that equity and use it as a financial resource. That's a difference in the housing market between then and now, and something most people didn’t have access to during the housing crisis for example. If folks had more equity in their homes the housing crisis probably wouldn't have been such a crisis.

You know, if we look across the country, this $56,700 in average gain, you see it, depending on the state you’re in. Of course, we talked about it being high here in California. It’s $119,000. Think about that. You know, somewhere in the middle of the country, $22-24,000 in gain in the price of a home. That's the minimum as you can see. Oh sorry, North Dakota only clocked in at fifteen thousand. So, what's the average price of a home there? Two hundred thousand? Maybe. They still got a seven and a half percent return. Still a good, good thing for all you homeowners out there everywhere. Awesome really. Congrats! A report came out a couple of months ago saying "in every major city", listen to this. "In Every major city, it was cheaper to buy a home than to rent, when you consider the equity growth right now." Every major city.

Unfortunately, not a lot of great news out there for you first time home buyers. Rents have been skyrocketing. Certainly, home equity, is the benefit of owning a home, that many, many people enjoy. So, if you are one of those frustrated buyers, stay focused. Home equity is the brass ring, or reward, at the end of your quest. Not sure if that is a great analogy, but when I was a little kid we used to ride this merry go round at the beach. On this particular merry go round, they had this kind of ring dispenser. As you rode by on your horse, you could reach out and pull a ring from this dispenser on the last revolution of the ride. If you got lucky and pulled the brass colored ring, you could exchange it for a free ride. Quite satisfying, but It was a simpler time for sure. Anyhow, the point being, keep your eyes on the prize. Eyes on the prize.

CoreLogic's CEO said, “Not only have equity gains helped homeowners more seamlessly transition out of forbearance and avoid a distress sale, but they have also enabled many to continue building wealth." That’s what we were just talking about, the ability to build wealth through equity is one of the greatest benefits of home ownership. We know there’s a ton of non-financial benefits of home ownership.

I've talked about those extensively, and recently posted this video about those "Amazing Non-Financial Benefits of Homeownership". The concept of home has definitely grown in many people’s hearts and minds as we’ve gone through the pandemic. But the financial benefit of building wealth is a huge, huge opportunity in home ownership.

She goes on to say "U.S. households own $36.8 trillion in owner occupied real estate, $11.5 trillion in debt, and the remaining $25 trillion in equity. In inflation-adjusted terms, homeowners had an average of $294,000 in equity in quarter three of 2021 - a historic high." It’s unreal! The story on equity right now across the country in real estate is unreal. The average homeowner has $294,000 in equity.

This really is a great opportunity for all of you that have this benefit to tap into. So many opportunities here with your home equity. You could sell your home for record high profit, leveraging the current housing inventory crisis, and extreme seller's market that we current find ourselves in. That upper hand, if you will, paired with your amazing gain in home equity over the last couple of years, could put you in the perfect position to find, and purchase that exquisite dream home you've always desired. Or perhaps you've already been fortunate enough to secure your castle, but now the kids are grown or you've had your fill of parties and entertaining. Maybe at this point in your life you want something simpler, smaller, less square footage and yard to clean and maintain. I hear that. Instead of cashing in all that profit and home equity to buy something larger, you could find a smaller space to fit your needs, and then invest or save all that money for whatever comes next. Still loving where you live? Perhaps you are interested in cashing in some of that equity for some home improvement to make the home you love even better. What will you do with your home equity? Share with us in the comments below.

Where are mortgage rates headed? What about loan forbearance and the foreclosure crisis? Will home price appreciation continue? Answers to these questions and more...right here, right now!

Welcome back once again to our real estate market update! I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes Blog we cover topics related to buying and selling residential real estate, and trends happening across the housing market, with new posts every week.

Let's start with what you can expect for projections on mortgage rates. You can see here from Fannie, Freddie, National Association of Realtors, and the mortgage bankers association, what they are saying about 2022, broken down by quarter. You can see the averages for mortgage rates there for Q1, 2, 3, and 4. I’m not here to tell you this is where mortgage interest rates are going to be. I believe that’s a fools game. I’m going to always look at what the experts are saying, and I’m going to give you an expert opinion on this. What are they saying right now? Somewhere between three and a half and four percent, in the second half of the year for mortgage rates. So that is, incidentally, exactly where we are right now, seeing a massive drop on the average 30-year fixed rate home mortgage loan last week from 3.56% to 3.55%. Of course, I'm kidding. The mortgage rate barely moved, but we are in the predicted zone. We’re definitely experiencing an upward trend, with those interest rates increasing a full half point since the end of last year. Mortgage rates will continue to fluctuate up and down, up and down, but I believe they will continue to trend in an upward trajectory. I talked about this several weeks, and even several months ago. I think we’re going back to where we were with mortgage interest rates. The last ten years we’ve been between three and five percent with the average 30-year fixed home loan. Still great financing available. Great, great financing for a home. That’s what you can expect with mortgage rates if you're looking to buy a home or refinance an existing home loan. How do you think mortgage rates will shake out over the next eleven months? Leave your predictions in the comments below. I'd love to hear your thoughts!

Alright, mortgage forbearances have finally fallen below one million. Going into this year, I believe loan forbearance is going to be a non-issue for most people, and I don’t think we’re going to hear much about it. But I want to update you on it just the same. Just under a million, about 890,000 mortgages actively in forbearance. That represents about 1.6% of all active mortgages. And four out of five families that are coming out of mortgage loan forbearance, are coming out either having worked out at payment plan with their lender, or having paid off their back payments. There are people that still will need to do something, but it’s a very small fraction. And, by the way, their homes have appreciated on average, over $57,000 in the last year. So, they do have opportunities and options because of that. How does all this affect you if you aren't dealing with loan forbearance yourself? It may not affect you at all, but if you are a potential home buyer, sitting on the sidelines and waiting for a big housing crash, or foreclosure crisis, so you can get an amazing deal on a home...that's probably not going to pan out. It's likely akin to the financial strategy of using the lottery to accumulate wealth, at this point in time.

The folks at CoreLogic say this. “We may see a little bit of an uptick in the foreclosure rate in 2022. Just an uptick though, from an extraordinary low level, we’re not expecting to see big increases.” Listen to this. “We expect delinquency rates overall on home mortgages to actually continue to remain quite, quite low.” So, in case you missed it, what’s going to happen with foreclosures this year? According to CoreLogic, they will remain quite, quite low. Again, I don't see forbearance or foreclosures being a big issue this year, because there are options for homeowners. I don’t see banks being in a posture trying to foreclose on people right now. I think they’re trying to work whatever out they can, and the numbers just aren’t there, like the last housing crisis. Please don't suffer in silence. If mortgage forbearance has you tied up in knots, reach out to me, using my contact info in the description below, and I'll do my best to help you.

Another question is, what’s going to happen with home prices here in San Diego? Has home pricing peaked? We drilled down on this last week, and I want to touch on it again, because it's important to see just how this is shaping up. I’m using this graphic here to show you input from the Federal Housing Administration, CoreLogic, and Case Shiller. This is a look at home pricing going back to January of 2021, all the way through October and November of last year. So, let me break this down for you, because the title here is, Has Home Price Acceleration Peaked, question mark? So, start out in January. The funny thing about this graphic is we’re starting out at 10%. We’re starting out at historical high home appreciation, and we’re, actually rising each month. So, this is a measure of year over year. So, what each one of these organizations does, is in January of this past year, they look at January 2021 home price appreciation as compared to January 2020, and what did home prices grow by. And we know in 2020 they grew by about 10%. And then each month it goes on. They record those for the other month. Now, we said home prices appear to look like they’ve peaked. And they do. But here’s the question. Have they peaked, or have they plateaued? I want to put that question on the table, because that’s what we're looking at right now. All the other experts out there are wondering this as well. Let me be very, very clear about that. I do think there has been a peak. But is it a plateau that we’re about to see? I’ll tell you this. I don’t think we’re going to see prices or home appreciation drop from 18 or 19% down to 5%. Now, I’m going to show you what forecasters are saying in just a minute. The average is about 5%. But I don’t think you’re going to go from 18% home price appreciation to 5% appreciation overnight, or in a year.

Home appreciation is still very, very strong in the housing market. We expect appreciation to continue in 2022. And if you look at those that are forecasting appreciation right now for 2022, the average is 5.2%. I just mentioned that. Anywhere from seven and a half to 2.8. Here’s one thing I see about forecasters right now. They’re already starting to up level their forecast. I think this average here of 5.2 is low. I think they’re going to go above that. But how much above that, I certainly don’t know. It’s anyone’s guess. But I think we’re going to see more than 5% home appreciation in real estate in 2022. And always remember, as home price appreciation goes down in this graphic, that’s not depreciation. It’s just less appreciation. And also remember, month over month, year over year, that home appreciation is cumulative. So, if you are a homeowner, you didn’t miss anything. We’re just seeing less appreciation than what we saw last year. You know, the word that’s often used in this is deceleration in appreciation, which means it’s coming at a slower rate. Think about a car going down the road, decelerating. Still moving very fast. Just not as fast as you were moments ago. What do you think about home price appreciation? Are we headed off a cliff, or is the sky the limit for home prices here in the San Diego housing market? Let us know in the comments!

I think as we look at mortgage rates, we look at loan forbearance, we look at home prices, we look at all the things happening in the housing market, CoreLogic does a nice job of summing up the bottom line: "So overall 2022 will be another strong year for housing. All be it a little bit higher mortgage rates, and we do think home sales will continue to rise, and actually reach a 16 year high in 2022." So, across the country we are seeing a lot of things happening in real estate. We need more housing inventory, and home buyers are in full force, like I talked about last week. Overall though, it looks like a very good real estate market coming up in 2022 for many of you.

The Top Indicator if You Want To Know Where Mortgage Rates Are Heading

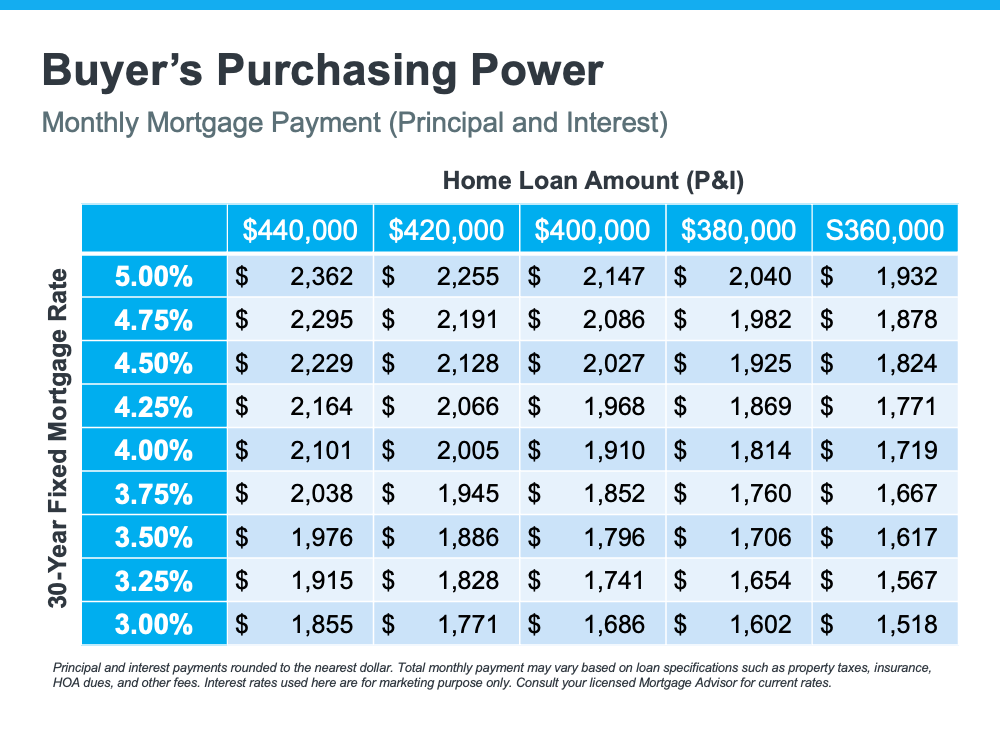

Mortgage rates have increased significantly since the beginning of the year. Each Thursday, Freddie Mac releases its Primary Mortgage Market Survey. According to the latest survey, the average 30-year fixed-rate mortgage has risen from 3.22% at the start of the year to 3.55% as of last week. This is important to note because any increase in mortgage rates changes what a purchaser can afford. To give you an idea of how rising mortgage rates impact your purchasing power, see the table below:

How Can You Know Where Mortgage Rates Are Headed?

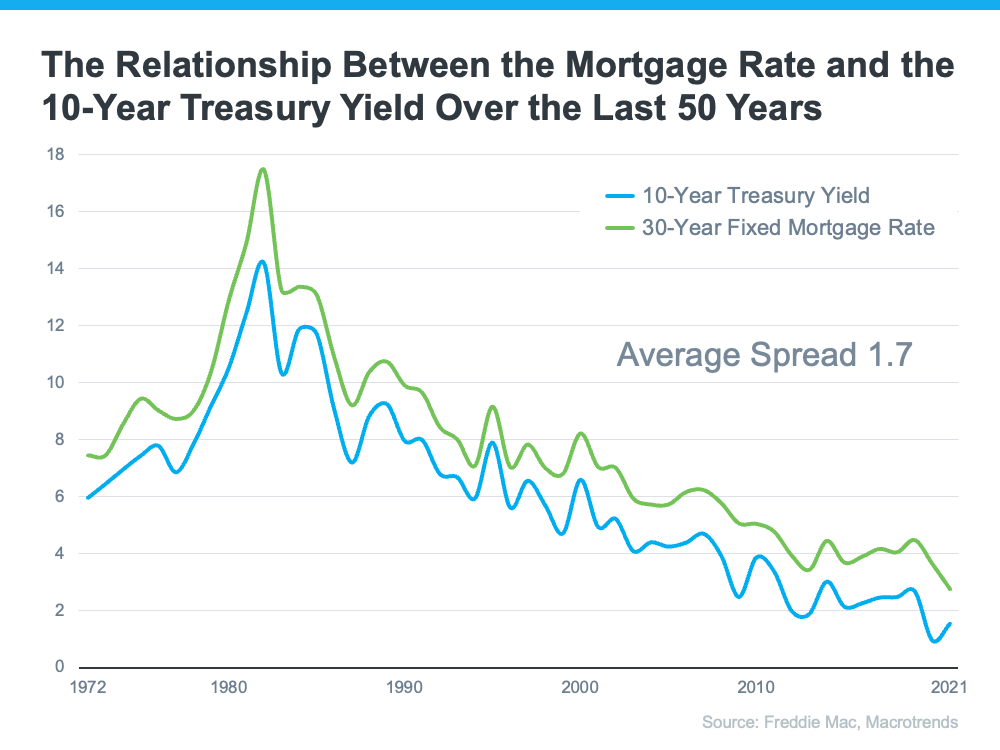

While it’s always difficult to know exactly where mortgage rates will go, a great indicator of where they may head is by looking at the 50-year history of the 10-year treasury yield, and then following its path. Understanding the mechanics of the treasury yield isn’t as important as knowing that there’s a correlation between how it moves and how mortgage rates follow. Here’s a graph showing that relationship over the last 50 years:

This correlation has continued into the new year. Pretty remarkably similar, huh? The treasury yield has started to climb, and that’s driven rates up. As of last Thursday, the treasury yield was 1.81%. That’s 1.74% below the mortgage rate reported the same day (3.55%) and is very close to the average spread we see between the two numbers (average spread is 1.7).

Where Will the Treasury Yield Head in the Future?

With this information in mind, a 10-year treasury-yield forecast would be a good indicator of where mortgage rates may be headed. The Wall Street Journal just surveyed a panel of over 75 academic, business, and financial economists asking them to forecast the treasury yield over the next few years. The consensus was that experts project the treasury yield will climb to 2.84% by the end of 2024. Based on the 50-year history of following this yield, that would likely put mortgage rates at about 4.5% in three years.

While the correlation between the 30-year fixed mortgage rate and the 10-year treasury yield is clear in the data shown above for the past 50 years, it shouldn’t be used as an exact indicator. They’re both hard to forecast, especially in this unprecedented economic time driven by a global pandemic. Yet understanding the relationship can help you get an idea of where rates may be going. It appears, based on the information we have now, that mortgage rates will continue to rise over the next few years. If that’s the case, your best bet may be to purchase a home sooner rather than later, if you’re able.

Bottom Line

Forecasting mortgage rates is very difficult. As Mark Fleming, Chief Economist at First American, once said:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

However, if you’re either a first-time homebuyer or a current homeowner thinking of moving into a home that better fits your changing needs, understanding what’s happening with the 10-year treasury yield and mortgage rates can help you make an informed decision on the timing of your purchase. Give us a call at Braceland Homes 619-947-3560 to discuss if and when the time is right for you to buy a home.