Braceland Homes Inc. is an Escondido, CA real estate brokerage founded in 2018 by retired US Navy officer Erik Braceland (DRE 02059069). Erik launched his second career after several underwhelming experiences with REALTORS® he worked with to buy and sell his own investment properties while serving on active duty. His systems, processes, and strategies positively impact the way homes are sold, and the systematic trademarked approach he embraces, guarantees his clients' satisfaction and success.

6 Key Things To Avoid After Applying for a Mortgage

Once you’ve found your dream home and applied for a mortgage, there are some key things to keep in mind before you close. It’s exciting to start thinking about moving in and decorating your new place, but before you make any large purchases, move your money around, or make any major life changes, be sure to consult someone like me, or the expert mortgage brokers we partner with at Braceland Homes – someone who’s qualified to explain how your financial decisions may impact your home loan.

Here’s a list of things you shouldn’t do after applying for a mortgage. They’re all important to know – or simply just good reminders – for the process.

1. Don’t Deposit Cash into Your Bank Accounts Before Speaking with Your Bank or Lender.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan originator.

2. Don’t Make Any Large Purchases Like a New Car or Furniture for Your Home.

New debt comes with new monthly obligations. New obligations create new qualifications. People with new debt have higher debt-to-income ratios. Since higher ratios make for riskier loans, qualified borrowers may end up no longer qualifying for their mortgage.

3. Don’t Co-Sign Other Loans for Anyone.

When you co-sign, you’re obligated. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

4. Don’t Change Bank Accounts.

Remember, lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your mortgage loan originator.

5. Don’t Apply for New Credit.

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be impacted. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

6. Don’t Close Any Credit Accounts.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants of your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. The best plan is to fully disclose and discuss your intentions with a qualified mortgage professional before you do anything financial in nature. Call or text me anytime 619-947-3560.

What are these rising interest rates going to do to home prices? Will they be affected at all? Let's find out!

Welcome to another REAL ESTATE MARKET UPDATE. I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes Blog we cover topics related to buying and selling residential real estate, and trends happening across the housing market.

Let’s talk about mortgage interest rates. Probably one of the biggest topics that’s going to be talked about, as we go into the new year. Real quick before we start, whenever I'm talking about a rate...and I may say interest rate, mortgage rate, mortgage interest rate...it's all the same thing. I'm simply referring to the rate of interest on a home loan in a general sense.

So, what’s going on with mortgage rates? The overall outlook is that mortgage interest rates are going to rise. I’ll talk about that, but this is a look right now, at the 30-year fixed home loan. If we look at January of 2020, prior to the pandemic, we're knocking on the door of 4 percent. Right now, the average 30-year fixed is 3.1 percent. Many calling for that rise going into next year. I’ll show you what forecasters are saying, but if you were to ask me what’s going to happen with interest rates, I think we’re going to go back to where we were.

This is a historical perspective on mortgage rates. Looking at 2016, ‘17, ‘18, ‘19, four really, I’m going to call them normal years in real estate, and we balanced somewhere between three and a half and five percent. I think we’re heading back there. I think we’re heading back into an environment of much more normal interest rates. We’ve seen some phenomenal mortgage rates over the last year or so. Historically low mortgage rates on a 30-year fixed mortgage loan, and I think we’re going to head back into a time where we were prior to the pandemic. Now you know in the real estate business, many people often ask "what’s the impact of rising mortgage rates on home prices and home sales? And if mortgage rates rise, how will the housing market be impacted?" Well, I went back and took a look at the impact on an environment of rising interest rates on home prices and home sales, so let’s see.

First one. Home prices are slightly impacted by rising mortgage rates. This is a look going all the way back to 2000 and what you see in the line graph there, the yellow and red, is the interest rate, and what you see in the bar graph, the blue and orange, is appreciation or depreciation during the housing crisis. The quick thing I want to point out is, in each rising interest rate environment represented by the red sections of the line, there’s no depreciation. Except during that housing crisis. When you start to look at rising interest rate environments, the first one in 2005 with less appreciation in 2006, but there is still home price appreciation over the previous year, meaning higher home prices. You look at 2012, 2013 and 2014. Again, an environment of rising interest rates, with varying levels of home price appreciation, but all with pretty substantial gains in home price appreciation and rising home prices. The next one, in 2016, 2017 and 2018. We go up and come back down a little bit, but still all with decent home price appreciation. Price appreciation is resistant to rising mortgage rates, meaning home price appreciation doesn't soften just because mortgage rates are rising.

Here’s why. Mark Fleming, sums this up best. “Home price appreciation is resistant to rising mortgage rates, primarily because most sellers would rather withdraw from the market than sell at lower prices, a phenomenon we refer to as downside sticky.” So, somebody is going to say okay, if I can’t get as much for my home, or if my home is not appreciating as fast, we’ll just take it off the market, that’s what's happening there. The other question is home sales, are they impacted by rising mortgage rates?

If we go back, all the way back to 1999, which is what you see in this graphic, we again have mortgage rates in the line graph and home sales in the bar graph. We can see home sales are NOT impacted by rising mortgage rates. Now I won’t walk you through each scenario, but you can see on here, each one of the red bars being rising interest rate environments, and they’re not corresponding with lower home sales. So, if you home sellers wanted to argue that its becoming a bad time to sell your home because interest rates are rising, I'd simply ask, on what information are you basing that opinion? Because when you go back and look at it historically, it just doesn’t prove out.

I want to wrap up with this quote, "Context matters right now for the housing market and certainly for purchase demand. The economy is improving, and millennials continue to age into your prime home buying years in large numbers, so context remains good for the housing market." Real quick for you home buyers, My oldest son is included in this millennial group, and he is super excited to be closing on his first home here in the San Diego housing market. I did help him find the home, and I represented him during the negotiations. It wasn't all good times. We did have to compete against multiple offers. We didn't get a deal on the price because of that. We got very little in seller concessions, and my son has some work to do to get the home up to the standard he'd like it to be at. So, I know it's tough out there for you home buyers, and that's the reality of the housing market still, in many areas of the country, just like here in the San Diego housing market. But you know what? It was still a win for my son. We got the home that he wanted. And he can make it the way he wants it, as time and budget allow. That's the goal, so persevere and don't give up. Get your foot in the door to home ownership now. The context of the housing market remains good for you too. Was it better yesterday? Probably, and I'm sorry you missed out on that. Stop waiting. I think overall, as we look at mortgage interest rates, we can expect an environment of rising interest rates going into next year. I don’t see that affecting the housing market dramatically, but it will cost more for those of you looking to buy a home. I think you should expect that, as we go throughout the next several months and the next year, but leave me a comment below and tell me what you think. Perhaps I'm missing something. Please let me know!

How do you predict mortgage rates will impact the housing market? Will home price appreciation take a hit? What will be the effect of rising mortgage rates on home prices? A lot to consider for sure. Leave me a comment below and tell me what you think.

If you’re thinking of buying a home, you’re probably wondering what you need to save for your down payment. Is it 20% of the loan, or could you put down less? While there are lower down payment programs available that allow qualified buyers to put down as little as 3.5%, it’s important to understand the many perks that come with a 20% down payment.

Here are four reasons why putting 20% down may be a great option if it works within your budget.

1. Your Interest Rate May Be Lower

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll End Up Paying Less for Your Home

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your Offer Will Stand Out in a Competitive Market

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You Won’t Have To Pay Private Mortgage Insurance (PMI)

What is PMI? According to Freddie Mac:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner's insurance. It's a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you've built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a larger down payment on a new home.

Bottom Line

If you’re looking to buy a home, consider the benefits of 20% down versus a smaller down payment option. Call us at Braceland Homes 619-947-3560 so you have expert advice to help make your homeownership goals a reality.

To succeed as a buyer in today’s market, it’s important to understand which market trends will have the greatest impact on your home search. Danielle Hale, Chief Economist at realtor.com, says there are two factors every buyer should keep their eyes on:

“Going forward, the conditions buyers face are primarily dependent on two things: mortgage rates and housing supply.”

Here’s a look at each one.

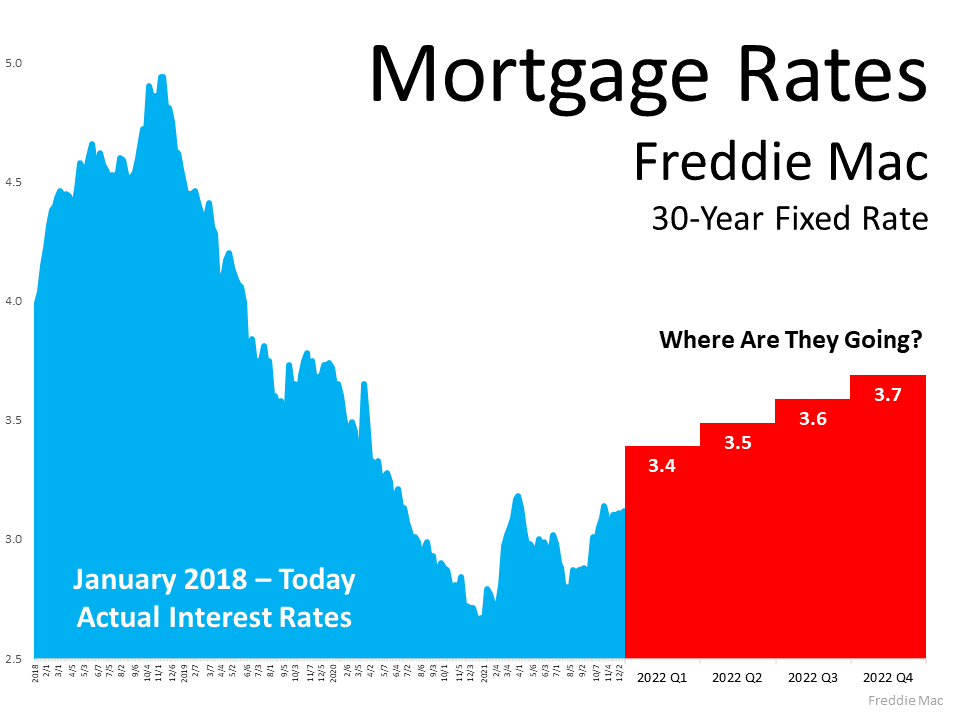

Mortgage Rates Projected To Rise in 2022

As a buyer, your interest rate directly impacts how much you’ll pay on your monthly mortgage when you purchase a home. Mortgage rates are beginning to rise, and experts forecast they’ll continue going up in 2022 (see graph below):As the graph shows, mortgage rates are expected to climb next year. But they’re still low when you compare to where they were just a few years ago. That presents today’s buyers with some motivation to lock in a low mortgage rate before they climb higher.

More Homes Are Expected To Be Available This Season

The other market condition buyers need to monitor is the number of homes available for sale today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows the current supply of inventory sits at just 2.4-months. To put that into perspective, a 6-month supply is ideal for a balanced market where there are enough homes to meet buyer demand.

However, there may be good news for buyers who are waiting for more options. A recent realtor.com survey shows more sellers are planning to list their homes this winter, meaning more choices will likely be available soon.

What Does That Mean for You?

Even if your options improve some this season, it won’t significantly shift market conditions overnight. According to NAR, many more listings need to be available to move closer to a more neutral market:

“Given the average monthly demand . . . , 3.55 million homes should be on the market to meet a level of inventory equal to six months of demand, implying a shortage of homes for sale of 2.24 million.”

So remember, even with more homes expected to come to market this season, competition among buyers will remain fierce as there still won’t be enough homes for sale to meet the current demand. That means you’ll need to act quickly when you’re ready to make an offer.

Check out or recent video: Expected Inventory Increase in the Housing Market This Winter?

Bottom Line

If you’re planning on buying a home this winter, more options are welcome news, but it doesn’t mean you should slow down. Give us a call at Braceland Homes 619-947-3560 today so you have an expert on your side to help act as quickly as possible when the right home for you hits the market.

Real Estate Market Update December 2021 | Erik Braceland

Mortgage rates, home prices and sales oh my. Let's take a look at what's trending with these subjects and a few others

Welcome to another REAL ESTATE MARKET UPDATE. I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes channel we cover topics related to buying and selling residential real estate, and trends happening across the housing market.

Here are some projections on mortgage rates from four of the leading providers of information on mortgage rates; Fannie, Freddie, Mortgage Bankers Association and National Association of Realtors. What are they saying? Sometime between the middle and the end of next year, they're forecasting between three and a half and four percent, on the average 30-year fixed home loan. So, as I've been saying, it’s going to cost more to buy a home, and I think you should expect mortgage rates to rise. Now I’m not here today with a crystal ball to say this is what mortgage interest rates are going to be, but I am here to say I think we can expect an environment of rising mortgage rates.

A lot of people are concerned and asking "what’s going to happen to home prices in 2022?" Well, forecasters are predicting an average 5.1 percent rise in home price appreciation next year. You can see anywhere from seven and a half to almost 3 percent home price appreciation on the low side. This is a direct nod to seeing more inventory coming to the housing market. The price will always be dictated by supply and demand in any market. And, as such, holds true for the housing market as well. That's what we can expect relative to home prices in 2022. Basically, a continuation of our current housing market environment going into next year. Other questions that may be on your mind at times, "is the housing market going to crash?" And many of us concerned about all we’ve seen over the last few years, or the last 20 years for that matter. "What about mortgage forbearance? How will those mortgage forbearance plans factor in to all this?" The short answer is, don't worry, the housing market is not going to crash regardless of what all those clickbait thumbnails on the internet claim. But let's take a look at projected home sales.

The bottom line here, is that home sales for 2021 are forecasted to continue increasing throughout the year. 2022 home sales are predicted to be even stronger. I want to remind you that last year in 2020, over six and a half million homes sold in this country. We’re forecasted to sell more than that this year, and even more than that next year! The past two years, have both been phenomenal years in the real estate market, with an even better year predicted in home sales for 2022 as well.

This graphic really does a great job to show just where we’re at in the housing market based on months of housing inventory in this extreme seller’s market that we’re in right now. Let's quickly talk about buyer's market vs seller's market. I've talked about this before, but a simple way to understand this is that six months of housing inventory is kind of the sweet spot where we have a neutral market. Above six months of housing inventory creates a buyer's market. Below six months of housing inventory creates a seller's market like we're in right now. Some markets, like our san Diego housing market, never really climb out of the seller's market because homes are in such high demand. Something about the weather. The beaches. I don't know. Anyway, thinking about selling your home? There has literally never been a better time! Sometimes I feel like a broken record saying that, but it's just the truth. This visual just underscores that. I know my big fat head is in the way, but it shows all the way back to 1999, where it was also a seller's market. But then housing inventory hovered around five percent. Now it is consistently under three percent, and it’s just been a great seller’s market for those that have decided to sell, and that continues today.

Now I want to touch quickly on home equity and home appreciation. For you home owners out there, this is all about the ever-increasing value of your home, but bear with me for just a moment while I address our home buyers. What advice do I have for you home buyers that say, "I really don't want to buy at the top of the housing market"? Well, I certainly do understand why you might feel like we're at the top of the market because homes are so expensive. That is not an uncommon feeling, and the best time to buy a home, is right now. But I do want to qualify that statement with this one, now is the best time to buy a home if it is also the right time for you and your family to make a move. I'll always go back to that. Forget about what the market is doing, and first consider the needs of you and your family. That should always come first. The next best time to buy a home is...as soon as possible, if it can't be right now because things homes are just getting more expensive. Price increases and mortgage rates are conspiring against you. This visual representation of a recent home price expectation survey, based on the national average priced single-family home, Shows the projected home appreciation for that home, if it was purchased this year, all the way through 2026. Let's look at this. What kind of appreciation is at stake here? A hundred and eleven thousand dollars! Just over $111,000 in real home appreciation over the next five years on a $350,00 home! Wow! Where else are you going to get a return like that? And that's just the gain on home appreciation and increased home equity! Did I mention you'll be living in that home, and paying down the fixed payment on your mortgage loan, instead of paying an ever-increasing rent payment towards your landlords mortgage loan, all while your home equity magically appreciates all by itself?

While we don't have time to go into all the other benefits of homeownership right now, I did just shoot a recent video on some of the non-financial benefits of homeownership that I'll link to in the description. So, check that out, but it really is a good time to go out and buy a home.

I want to conclude this week's update with a little inspiration. All of us lead busy lives to some extent or another, and this time of year can be even busier for many of us, just always going, going, going. Take some time over the next few weeks to rest with your family and friends as this year comes to a close. Don’t get lazy and take all of that time, but take the time you need to rest and relax. Sir James Tyson said this, “The moment you feel most tired is the moment you must accelerate, because that’s when everybody else is feeling tired as well...but if you can break through that pain barrier you can achieve great things." This time of year, is a great time to do that because you can accomplish it without too much pain or sacrifice. Here's how; take some time off if you can, but set aside some of that time off towards the end to get a jump on next year. I think you'll find it helpful to begin the year with a head start and a little extra momentum. If you begin 2022 strong, you will carry that momentum throughout the year.

That's it for now. I'm Erik Braceland for this edition of our Real Estate Market Update. And from everyone here at Braceland Homes, thanks for joining me, and thank you for the time that you spend to be aware of what's happening in our current housing market. You will enjoy a better, more successful real estate experience because of it!

If you've enjoyed this content or found it helpful, please tell me in the comment section below. I'd love to hear what you think. And don't forget to share this content with someone you think might be interested.

Homebuyers Are Going on a Shopping Spree This Winter

Black Friday and Cyber Monday are over, which means some shoppers have wrapped up their holiday buying. But there’s still a group of buyers that are very active this holiday season – homebuyers.

Experts anticipate the real estate market will see a flurry of activity this winter, and that’s great news for today’s sellers. If you’re planning on listing your home, there’s no need to wait until the spring for better conditions – today’s real estate market is already heating up.

Buyers Have Warmed Up to the Idea of Purchasing This Winter

The past 18 months brought about significant lifestyle changes for many of us, including the rise in remote work, job changes, and even early retirement for some. For many people, it’s prompting a search for their next home now rather than waiting for warmer months.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), points out how this winter may see a significant number of sales:

“Compared to other past winter seasons, this winter season’s sales activity will be stronger. . . . This winter, there will be more sales compared to pre-pandemic winters going back all the way to 2006.”

You might be wondering: what does strong sales activity mean for you? It means there are likely to be more buyers active in the market this winter – far more than more normal, pre-pandemic years.

In the same article, Danielle Hale, Chief Economist for realtor.com, puts it in these simple terms:

“Sellers can expect to see plenty of buyers.”

The more buyers there are in the market, the more likely it is your home will get noticed. That can lead to a multiple-offer scenario or a potential bidding war. Receiving multiple offers on your home means you can select the right offer and terms for your situation – so you can truly win as a seller when you list your house this winter.

Bottom Line

If you’re thinking about selling your house, you don’t need to wait until the spring. Buyers are ready now. Let’s connect at Braceland Homes call us at (619) 947-3560 to discuss why selling this holiday season could be the gift that keeps on giving.

Everybody wants to know... should we expect an inventory INCREASE in the Housing Market this winter? Let's find out!

Welcome to another Braceland Homes REAL ESTATE MARKET UPDATE. I’m Erik Braceland with Braceland Homes here in sunny San Diego, California, where we guarantee the sale and/or purchase of your home. Here on the Braceland Homes channel we cover topics related to buying and selling residential real estate, and trends happening across the housing market.

To kick this off I want to address a question that's been top of mind for many of us. Is this housing market returning to normal? A recent Wall Street Journal article asks "will real estate ever be normal again?" Probably a better question to ask right now is, "will real estate ever return to normal?", because the housing market is still anything but normal. I want to talk about what we're likely to see relative to those thinking about listing their homes.

If we go back and look at a normal market, when do homes normally start to appear in greater quantities in the housing market? In a normal housing market, we would say in the spring selling season of April, may, June. But again, this year is anything but normal, and I want to make that clear. In this market, it's going to be this winter where we begin to see an increase in home listings. It going to be those home sellers that been thinking about selling, waiting for the right time, that finally say "this is it!" There have been a conclusive number of surveys that show a high percentage of home owners are saying that now is the right time to sell a home. So I want to break that down for you here, and share some very interesting information from the national association of realtors.

I'll start with this quote from the folks at the national association of realtors. They say "home sellers have historically moved when something in their lives changed – a new baby, a marriage, a divorce or a new job...but the pandemic has impacted everyone, and for many this became an impetus to sell and make a housing trade." So normally life events drive our major decisions, and shape our lives. Your dream may have been to live in a condo downtown and enjoy all that lifestyle includes. Then BOOM! Along comes this pandemic. Then suddenly your dream is NOT to be downtown with all those other people in such close proximity. Perhaps now your dream is to move to the suburbs, or even the mountains, and put a little more distance between you and your family and everyone else out there. Now a lot of people made a lot of decisions about housing for a lot of different reasons over the last year or two, but its safe to say the pandemic drove a lot of those decisions rather than life events.

In that same report that continue on to say " the pandemic likely spurred occupants to shorten their home stay, as tenure in the home decreased to eight years to ten years, according to the report. This is the largest single-year change in home tenure since the national association of realtors began collecting such data". I'm going to share a visual of that, but I just wanted to explain that most of us in the industry, and even many of you have always been taught to believe that the majority of people move every five or six years.

As you can see here from 1985 until 2008 folks were indeed staying in their homes for an average of 6 years. Post 2008 you can see the average tenure of homeownership began to climb from six years to seven, eight, nine, and even ten years more consistently in the last few years with an average tenure of 9.2 years from 2008 to 2021. Lots of different reasons for that, but now in 2021 you see this drop down to only 8 years. Very, very interesting. Couple of things here, and I'm not suggesting that a single year constitutes a trend. What I am saying, is that there a lot of people that have been living in their homes for a decade or longer. I'm saying there is a lot of pent up demand for home owners to sell and change their living situation. Perhaps they have been unable to sell for any number of reasons, including, but not limited to, not having adequate equity available in there home to sell for a profit or to break even. Now they do have that equity, and the rapid price appreciation we've seen this year has been the driving factor in that for many home owners. And that brings up a great question for you home owners. Do you know how much your home is worth given the recent home price appreciation?

I do have some opinions on how to find out in this video titled "27 Home Selling Tips To Sell Your Home Fast And For Top Dollar"

But if we start to look at the different factors we've been discussing recently, including the increased importance and emphasis on the concept of home for people, and the increased tenure in those homes, that all lends itself to the scenario where folks begin telling themselves that now IS the right time to make a move. Let's take a look at this quote from realtor.com "the pandemic has delayed plans for many Americans, and homeowners looking to move on to the next stage of life are no exception. Recent survey suggest the majority of prospective sellers are actively preparing to enter the market this winter." Pretty interesting. All the research that they're doing over there suggesting that the bulk of prospective home sellers are gearing up to market their homes over the next several months. Now we know in a normal housing market, sellers, over the last decade or two, have typically taken these winter months to prepare for those spring home sales. But it looks like many sellers are going to jump off this winter and say "now is the time".

We see here that of those sellers that plan to list this winter, 93% have already taken steps toward listing their home, including working with an agent. 65% have already listed their homes for sale or plan to during the winter months. 36% have researched the value of their home and other homes in their neighborhood. These folks have also begun making repairs and started the decluttering process. So many homeowners getting ready to sell right now. How about you? Have you thought of selling your home? Do you know what to do to get everything ready? How about buying a home? I know some of you will be looking for you first home, and others will be looking for a replacement home? This market is creating great opportunities for any and all of those options. I recently got a comment from a viewer on one of my videos comparing my optimistic perspective on the real estate market, as a real estate broker, to big tobacco trying to sell the consumer on the benefits of smoking. While I appreciate that viewer's perspective, I will continue striving to always show you the silver lining to the housing market, because there always is one. At the end of the day, unless you are making a long distance move to another area of the country with a much differently priced housing market, your home purchase or sale is going to be impacted very minimally by what the housing market is doing at any particular time. Most of us are making a move within the same city so if you sell high, you'll buy at those same inflated home prices negating any real gain or loss. The same goes in the other scenario. If you're buying for the first time when the market is high, even if you end up selling when the market is low, chances are, you'll also be buying that next home when the market is also low. Much more important than what the market is doing at a certain time, is if the time and circumstances are right for you and your family to make a move. Determine what you want and need, and then find a competent professional that can help you make it happen! If you're with me on this, consider subscribing to our YouTube channel so we can stay positive, and focused on our accomplishing our real estate goals together.

Alright, let's see what this report has to say about the top reasons folks plan to sell their 8homes this winter. 37% say their home no longer meets their needs. Maybe they've started working from home, so now they need an office. 33% have realized they want different home features after spending more time at home. Perhaps they want a gym to work out in at home to keep from going stir crazy while working from home, or to avoid the crowds at 24-hour fitness. 32% want to move closer to friends and family. Along with home, I believe the pandemic has also made family much more important and more of a priority to many of us. And finally, 23% are looking for a home office. I guess I jumped the gun on that when covering the home features, but it's clearly a thing. Many of us shifted to working from our homes on a permanent basis because of the pandemic. So again, many home owners ready to sell real soon, and these are some the top reasons driving those decisions along with record high home equity.

What's happening with current active home listing activity? We can see here that housing inventory is still well below what its been over the last five years. You'll see on top the more normal housing market years of 2017, 2018, and 2019 where housing inventory gradually climbs starting in the spring, peaks over the summer, declines during the fall, and then finally flattens out during the winter months. Last year we have a pretty steady decline as the pandemic wreaks havoc and sellers pull their homes off the market. What a mess! Then this year we start with a relative bang, but total housing inventory is still way below even what it was last year. Now that housing inventory has flattened out, and I predict it will continue to grow. Ideally inventory numbers will continue to grow for you home buyers so we can get out of this auction effect environment that we've grown accustomed to in many housing markets including my own San Diego real estate market. As we know, there is no shortage of home buyers out there which is great for you home sellers. I really do believe we are in for a bit of a leveling of the playing field with increased home listing activity in the near future, so watch for that.

Looking at the most recent data, the chief economist at realtor.com says this, "on a positive note, new listings this week were higher than we saw at this time one year ago, the first uptick in eight weeks." Again, we are starting to see more home listings come to the housing market. More folks are contacting us here at Braceland Homes every week for assistance with their home sales and purchases, and that's just another indicator that things are poised to take off this winter, so don't get left out in the cold.

Two Reasons Why Waiting To Buy a Home Will Cost You

If you’re a homeowner who’s decided your current house no longer fits your needs, or a renter with a strong desire to become a homeowner, you may be hoping that waiting until next year could mean better market conditions to purchase a home.

To determine whether you should buy now or wait another year, you can ask yourself two simple questions:

Where will home prices be a year from now?

Where will mortgage rates be a year from now?

Let’s shed some light on the answers to both of these questions.

Where Will Home Prices Be a Year from Now?

Three major housing industry entities are projecting ongoing home price appreciation in 2022. Here are their forecasts:

Fannie Mae: 7.4%

Freddie Mac: 7%

Mortgage Bankers Association: 5.2%

According to the National Association of Realtors (NAR), the median price of a home today is $353,900. Using an average of the three price projections above (6.53%), a home that sold for $353,900 today would be valued at $377,010 at the end of next year. As a prospective buyer, you would therefore pay an additional $23,110 by waiting.

Where Will Mortgage Rates Be a Year from Now?

Today, Freddie Mac estimates the average 30-year fixed mortgage rate in the fourth quarter of this year will be 2.8%. However, most experts believe mortgage rates will rise as the economy recovers. Here are the forecasts for the fourth quarter of 2022 by the three major entities mentioned above:

Fannie Mae: 3.4%

Freddie Mac: 3.8%

Mortgage Bankers Association: 4%

That averages out to 3.73% if you include all three forecasts. Any increase in mortgage rates will increase your costs.

What Does It Mean for You if Home Values and Mortgage Rates Increase?

If both variables increase, you’ll pay a lot more in mortgage payments each month. Let’s assume you purchase a $353,900 home in the fourth quarter of this year with a 30-year fixed-rate loan at 2.8% after making a 10% down payment. According to mortgagecalculator.net, your monthly mortgage payment would be approximately $1,309 (this does not include insurance, taxes, and other fees because those vary by location).

That same home one year from now could cost $377,010, and the mortgage rate could be 3.73% (based on the industry forecasts mentioned above). Your monthly mortgage payment after putting down 10%, would be approximately $1,568.The difference in your monthly mortgage payment would be $259. That’s $3,108 more per year and $93,240 over the life of the loan.

Add to that the approximately $23,110 a house with a similar value would build in home equity this year due to home price appreciation, and the total net worth increase you could gain by buying this year is over $115,000 (the $93,240 mortgage savings plus the $23,110 potential gain in equity if you buy now).

Bottom Line

When asking if you should buy a home, you may think of the non-financial benefits of homeownership. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year. Call Braceland Homes at (619) 947-3560 to discuss buying your next home and the financial benefits of buying now!

Struggling To Find a Home To Buy? New Construction May Be an Option.

There’s no question that the financial benefits of selling a house are outstanding today. Now is truly a great time to list if you’re ready to make a change. But if you do sell your house right now, you may be wondering where you’ll go when you move.

With so few homes available to buy right now, you might be considering building a new home as one of your options. But you may be unsure if that’s the way to go. Let’s compare the benefits of a newly built home versus moving into an existing one, and why working with one of our agents throughout the process is mission-critical to your success no matter what you decide.

The Pros of Newly Built Homes

First, let’s look at the benefits of purchasing a newly constructed home. With a brand-new home, you’ll be able to:

1. Create your perfect home.

If you build a home from the ground up, you’ll have the option to select the custom features you want, including appliances, finishes, landscaping, layout, and more.

2. Cash-in on energy efficiency.

When building a home, you can choose energy-efficient options to help lower your utility costs, protect the environment, and reduce your carbon footprint.

3. Minimize the need for repairs.

Many builders offer a warranty, so you’ll have peace of mind on unlikely repairs. Plus, you won’t have as many little projects to tackle. QuickenLoans puts it like this:

“Buying a new construction vs. existing home typically means you’ll have fewer repairs to do. It can be a huge relief to know that it’s unlikely you’ll have to repair the roof or replace the furnace.”

4. Have brand new everything.

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

The Pros of Existing Homes

Now, let’s compare that to the perks that come with buying an existing home. With a pre-existing home, you can:

1. Explore a wider variety of home styles and floorplans.

With decades of homes to choose from, you’ll have a broader range of floorplans and designs available.

2. Join an established neighborhood.

Existing homes give you the option to get to know the neighborhood, community, or traffic patterns before you commit.

3. Enjoy mature trees and landscaping.

Established neighborhoods also have more developed landscaping and trees, which can give you additional privacy and curb appeal. As Investopedia says, if you buy an existing home:

“Odds are, too, that the home will have mature landscaping, so you won't have to worry about starting a lawn, planting shrubs, and waiting for trees to grow.”

4. Appreciate that lived-in charm.

The character of older homes is hard to reproduce. If you value timeless craftsmanship or design elements, you may prefer an existing home. According to Houseopedia:

“Charm is priceless. Existing homes, especially those built in the 1950’s or before, often offer architectural elements, historic charm and a quality of craftsmanship not available in new homes.”

The choice is yours. When you start your search for the perfect home, remember that you can go either route – you just need to decide which features and benefits are most important to you. Working with the guidance our team will help you make the most informed and educated decision, so you can move into the home of your dreams.

Bottom Line

If you have questions about the options in your area, call Braceland Homes at (619) 947-3560 and let’s discuss what's available and what's right for you, so you’re ready to make your next move with confidence.

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

The ability to save for a down payment

The ability to qualify for a mortgage at the current lending standards

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

What Is the Difference Between a Conforming Loan and a Non-Conforming Loan?

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

What Difference Does It Make to Me as a Home Buyer?

A Forbes article earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

What Happened Last Week?

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Bottom Line

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Connect with Braceland Homes to discuss how these changes may impact you.